Safeguarding Australia's climate policies

The trifecta of carbon market sensitive elections is almost over

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below. By subscribing you’ll join more than 5,000 people who already read Carbon Risk. Check out the Carbon Risk backstory and find out what other subscribers are saying.

You can also follow on LinkedIn, Bluesky, and Notes. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 8 mins

In November I published an article highlighting the three carbon markets set to encounter electoral turbulence in 2025: Germany (its general election was held on 23rd February), Canada (voting takes place on 28th April), and finally, Australia (polls open on 3rd May).

In the aftermath of his election victory, Freidrich Merz, the next chancellor of Germany set a target of forming a new coalition government within eight weeks. It’s yet to be seen what policy chips have been traded by those hoping to form a government, as well as those left on the outside, such as the Greens, who may still be required to lend their support. Although any coalition is expected to include the CDU/CSU and the SPD, the implications for reform to Europe’s ETS1 and ETS2 are still uncertain. Germany’s response to the need for rearmament after America’s withdrawal from its defence role will be key (see Vollgas).1

The likelihood that Canadian Prime Minister Mark Carney will lead his party to victory in the forthcoming general election keeps on increasing. The leader of the opposition, Pierre Poilievre has vowed to drop the federal backstop to Canada’s industrial carbon pricing system. Prime Minister Mark Carney has signalled that he will protect it. The Liberal Party’s chances have swung from a less than 5% at the beginning of the year to 66% in the past week as opposition to Trump’s rhetoric and trade war north of the border has intensified (see Canada's industrial carbon pricing system should be protected).2

The third and final carbon sensitive election to take place in 2025 is scheduled for 3rd May when Australia heads to the polls. As in Canada the likely outcome of the election has switched 180 degrees in the space of a few weeks. In late February the opposition Liberal-National Coalition, led by Peter Dutton was the favourite to win the most seats. Dutton, much as Poilievre has in Canada, has been quick to mimic Donald Trump, even acquiring the nickname “Temu Trump”!3

It doesn’t seem to have done him any favours. The most recent MRV model published by YouGov indicates that the incumbent Labor Party are likely to win the most seats, but fall one seat short of forming a majority. The polls are still very tight and either party could yet eke out a win and lead at least a minority government.4

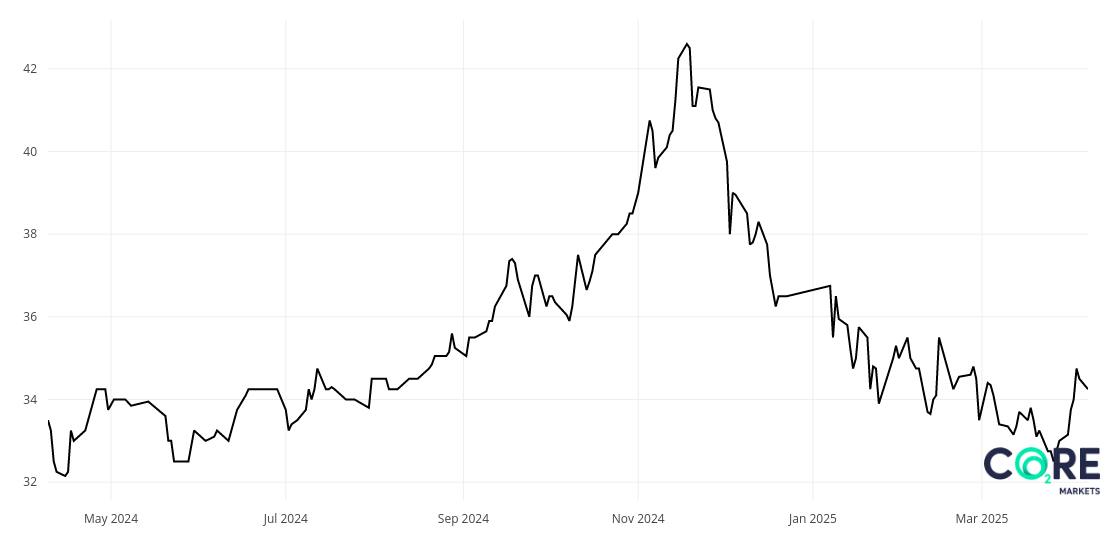

Before we take a look at Labor and Coalition climate policies, lets start off by looking at recent developments in Australia’s carbon market, the Safeguard Mechanism. The generic ACCU price jumped by almost 25% during the second half of 2024 to over A$42 per tonne. The carbon price had been bid up during 2024 as the first compliance period under the revised Safeguard Mechanism drew near. However, as the end of March deadline approached on the horizon, it was clear that obligated entities had sufficient cover to meet their compliance requirements.

The introduction of higher than expected volumes of Safeguard Mechanism Credits (SMCs) onto the market in late February added to the bearish sentiment. Remember that SMCs can be generated by obligated entities when they reduce emissions below their baseline, and can then be traded for example with entities who are above their own baseline (see The other side of the table).

Also contributing to the bearish market was a federal government decision to implement an amendment to the National Greenhouse and Energy Reporting Scheme (NGER) Act requiring operators of Australia’s open-pit coal mines to move from outdated state-based emissions factors, and towards site-specific methane sampling. Although the move is designed to capture under-reported methane emissions, weaknesses in the site-specific protocols means that emissions are likely to go down, rather than up according to RepuTex, reducing compliance demand for ACCU’s.5

Last years surge in the ACCU price has now completely unwound. However, end of year compliance trading and methane reporting protocols only tells us part of the picture. Political uncertainty has of course also had a major impact on the market. So how do the two parties compare, and what are the implications for the Safeguard Mechanism and the outlook for the ACCU price?