Vollgas

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 5,000 people who already read Carbon Risk. Check out the Carbon Risk backstory and find out what other subscribers are saying.

You can also follow on LinkedIn, Bluesky, and Notes. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 10 mins

There’s nothing like a crisis to focus minds on what matters!

The transatlantic rift over Ukraine’s future and the realisation that it no longer has the global policeman by its side has forced Europe to re-evaluate its place in the world. Yes, the signs were there months ago - perhaps long before 5th November - that the world is taking a different shape. However, it wasn’t until this past couple of weeks that the penny finally dropped that the end of Pax Americana was nigh.

European leaders have come together, not simply in a show of unity, but to plan a way forward that isn’t reliant on America. A bit like an understudy that comes out of the shadow of its mentor, Europe is rapidly asserting itself.

captures it well as he describes the “no-bullshit Europe” taking shape:1“The important thing is there has been a fundamental psychological change. US/Russian alignment has fixed European minds. This was an opening gambit involving national and EU budgets and EU borrowing mechanisms. In future, if things continue to deteriorate, it is likely to involve €200 billion in frozen Russian funds and a new €800 billion EU funding facility. They are not fucking about here. They are talking about seriously big measures. There is a sense of seriousness and clear-sightedness about Europe that has previously been completely absent.”

Defence spending by European Union member states is set to increase significantly in the next two years. Goldman Sachs baseline assumption is that the EU will gradually increase its annual defence spending by ~€80 billion by 2027 - equivalent to roughly 0.5% of GDP. Defence expenditures in the euro area accounted for 1.8% of GDP in 2024 and GS expects it to rise to 2.4% by 2027.2

The economic impact of defence spending depends on the type of expenditure and whether it is imported or produced domestically in Europe. GS estimates that additional spending will have a fiscal multiplier of 0.5 over two years, i.e. €80 billion will boost GDP by €40 billion. In response to the extra spending, GS have doubled their forecasts for German GDP growth: from 0.7% to 1.5% in 2026, and from 1% to 2% in 2027. If the rollout of defence spending can be fast-tracked then GS GDP growth could see an extra 0.3-0.5% boost per annum. In a recent column, John Authers of Bloomberg discusses the dramatic change in sentiment in Germany:

“Nobody doubts that this is the biggest turning point for German economic policy at least since reunification, and possibly much longer. The country’s frugal monetary and fiscal policies are born of folk memories of the Weimar Republic’s hyperinflation a century ago, and this is a decisive turn away from that.

Plenty of people predicted that Germany would have to start spending more; nobody I spoke to pretended to have had any idea of the scale of what is underway. Only a week ago, the talk was of €200 billion, which seemed extraordinary. Now we’re talking about €900 billion, closing in on the psychological threshold of $1 trillion.”

However, any deal that amends the constitution requires a two-thirds majority. It will be very difficult to achieve once the new Bundestag takes shape on 25th March and the far-right (who increased its share of the vote during the recent election), together with the far-left parties will be able to block the vote. It means the CDU-SPD coalition will need the support of the Greens to get their proposal through, but that will come at a price, and as

explains, it will probably mean the two largest parties have to devote much more funding in support of climate policies:3“The very least that would be required, therefore, is a fundamental reorientation of the CDU-SPD package in the order of hundreds of billions of euros, towards the priorities of the climate crisis. The CDU/CSU should be required to abandon their aim to rollback climate legislation and be forced to lay out a social safety net for the eventual introduction of the ETS2. De facto this would amount to a Kenya coalition agreement. If this cannot be done on the hair raising timeline apparently envisioned by the CDU-SPD negotiators, so be it. Nothing less should be the price that the Greens exact.”

As

outlines, Germany’s epochal change in approach to defence and security has opened the door to similarly big developments at the European level, while also enabling other EU member states to press for further growth. Denmark's Prime Minister for example has called on Europe to "spend, spend, spend" on defence:4“The European Commission last week proposed to change the EU’s fiscal rules to exempt defence spending, as Germany has done, which could unlock up to €650 billion of extra defence spending. At the same time, it proposes to establish a new fund that will allow member states to borrow up to €150 billion to spend on defence investment.”

Eurozone manufacturing activity remained in contraction during February according to the latest HCOB PMI survey but at 47.6 it is now at it’s highest level in two years. Expectations over future manufacturing growth also perhaps signal that a turning point could be on the horizon with manufacturers among their “most optimistic since Russia’s full-scale invasion of Ukraine at the start of 2022.”5

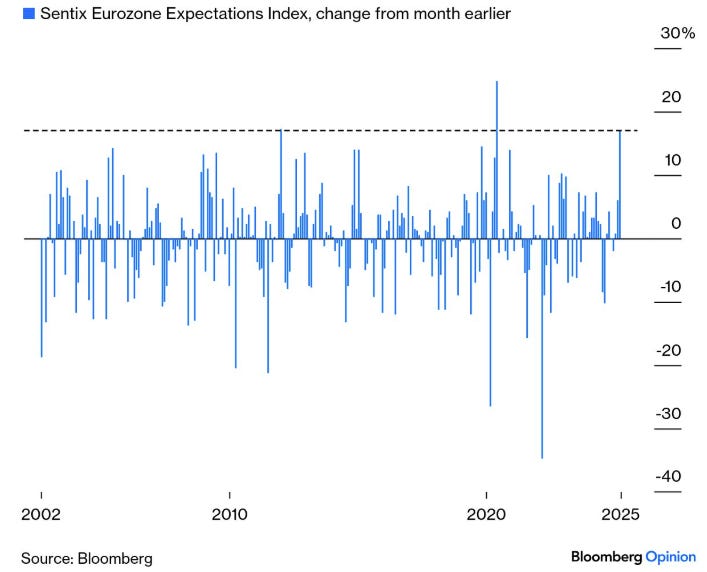

More recent data hints at the dramatic change in sentiment that has infected Europe’s business community. Expectations among eurozone firms experienced their second biggest ever month-on-month improvement according to Sentix. It was only the early pandemic rebound in expectations (the period following the initial lockdown) that prevents this latest rebound in expectations from being a record.

Back in September I warned that Germany’s manufacturing malaise was set to curb demand for EUAs. At the time everything was pointing towards an acceleration in the manufacturing downturn, while some of the largest industrial companies in Germany - Volkswagen, Intel, and others - were signalling that extreme measures would be required if their ongoing business in the country was to have a viable future.

Europe is now on the precipice of renewed economic growth, just not the growth it expected, or indeed wanted, but it is the one its got. Could the improvement in sentiment shake Europe’s industrial firms out of their myopia and force them to hedge against an impending deficit in EUAs? This could be the start, but there may be more, and this time from a more conventional source of demand for EUAs.