All-in on Brexit reset

Funds betting on early agreement to link UK and EU carbon markets may be disappointed

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below. By subscribing you’ll join more than 5,000 people who already read Carbon Risk. Check out the Carbon Risk backstory and find out what other subscribers are saying.

You can also follow on LinkedIn, Bluesky, and Notes. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 6 mins

UK Prime Minister Keir Starmer will hold a joint UK-EU summit on Monday 19th May, in what officials hope will reset Britain's relationship with the bloc five years on from Brexit.

Defence and security are expected to be top of the agenda as the UK and Europe look to fill the void left by America. More pertinently to readers of Carbon Risk there’s an expectation that the UK and the EU will agree to link their respective emissions trading schemes, the two sides hopefully committing to specific timeframe for the negotiations to be completed.1

As I discuss in Pegger thy neighbour: Why smaller carbon markets link up with larger cap-and-trade schemes, a linkage between the UK and EU ETS’ will improve liquidity, reduce costs, and lower carbon leakage risk. As in other arenas where countries agree to join forces, a linkage can also help to bolster investor sentiment. In this case the UK should benefit as investors perceive an increased commitment to ambitious climate policy:

“The act of linking your carbon market to a larger, more established market can be thought of as a country pegging its currency to the US dollar or a basket of currencies. By tying their hands, governments pursuing this strategy bolster their economic credibility with the market, often enabling domestic industry to benefit from lower capital costs than would be present otherwise.”

Industrial emitters in the UK have been lobbying the government to link up with the EU ETS for some time. Exporters are especially concerned that the relatively low carbon price in the UK will negatively affect their ability to remain competitive in Europe once the CBAM is gradually phased in from 2026. Many are worried that low carbon prices could have a detrimental impact on investment in technologies such as carbon capture and storage (CCS) that could help decarbonise UK industry.

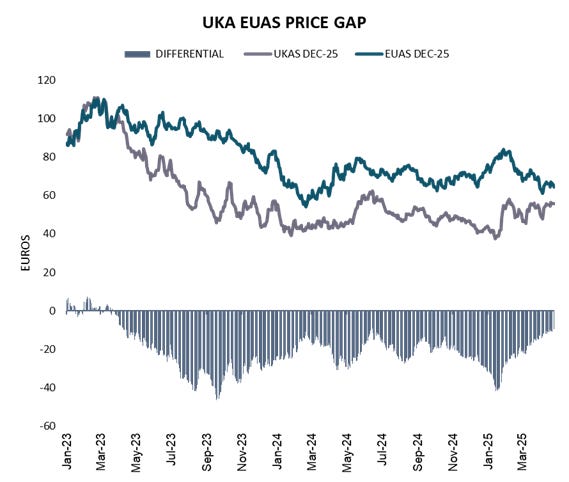

At the beginning of the year the UK-EU discount stood at 50%. The perception that the chances of a reproachment between the UK and the EU were fading, coupled with delays to the UK ETS reform process, sent the UKA price down to a record low of £31.54 (€37.35) per tonne (see Britain's green credibility gap: UK carbon price slumps to record low, 50% below the EU).

In late January the Financial Times published an article titled ‘Keir Starmer looks to link UK and EU emission trading schemes’. One senior UK government official is quoted as saying, “British business wants to avoid any kind of cliff edge or extra costs. We are looking for win-win solutions to build confidence and relinking our carbon markets falls into that category.”2

The UKA-EUA discount has narrowed sharply on the positive noises apparently coming out of Whitehall with the spread dropping to as low as 15% (~€10 per tonne) in recent weeks. However, more recent coverage from the FT on the UK-EU summit fails to mention the prospect of a carbon market linkage, perhaps indicating that the UK government are going cold on the idea, or at least are reigning in their public statements on the issue as negotiations draw near.3

Not everyone is in favour of carbon prices, whether that be the UK’s or the EU’s. Sir Jim Ratcliffe, founder of chemical giant INEOS, recently claimed that his Grangemouth petrochemical site faces a UK ETS charges totalling £15 million for its emissions during 2024. The Brexit supporter has slammed the UK’s net-zero policies as unaffordable and claimed that the carbon price is “killing manufacturing”.

Uppermost in the minds of the Labour Party is the strong performance of the Reform Party in the local elections in early May. The Reform Party is currently the joint favourite to become the largest political party after the next general election (scheduled to be held no later than 15th August 2029). It’s an astonishing feat for a political party that was only founded four years ago.45

Reform’s leader Nigel Farage has described net-zero as “lunacy”, suggested that “We should scrap the net-zero targets”, and in a sign that Farage already knows that climate scepticism is his next crusade recently said, “This could be the next Brexit, where parliament is so hopelessly out of touch with the country.”

Back in June 2019 the UK became the first major economy to commit to meeting net-zero by law by 2050. It prompted barely a murmur of opposition among the country’s politicians. Not so now. While the incumbent Labour government know that linking the UK and EU ETS’ together is in the country’s national interest, the potential for Reform — the likely opposition party — to make political capital from it is high.

The government face another delicate balancing act - between President Trump and America on the one hand, and Europe its closest neighbour and biggest trading partner on the other. The UK risks being caught in the middle as it seeks to tread the narrow path towards a securing a strong trade deal with the former, and a closer relationship with the latter. The risk is that the UK comes out with a bad deal on both accounts, with a linkage between the two carbon markets a potential casualty of a trade deal with America.

Investment funds are laser focused on the 19th May, hoping that both parties will signal their commitment to a linkage with a firm and preferably short timeline to complete the negotiations. Since the positive FT article was published in late January, investment funds have more than doubled their net long position to almost 20 million UKAs.

No one wants to see a repeat of Switzerland’s ETS linkage travails. Beginning in 2011, it took 6 years to finalise negotiations on linking the two schemes, but it wasn’t until 2020 that the linkage actually became operational. There’s no reason that a UK-EU linkage should take anywhere near that long, but with a Euro and net-zero sceptic party breathing down the neck of the establishment, and only four years to the next election, both sides really need to get a move on.

👋 If you have your own newsletter on Substack and enjoy my writing, please consider recommending Carbon Risk to help grow this amazing community of readers! Thank You!👍

Repost: Commitment issues

Almost twelve months to the day since I published this article, the price of UK emission allowances (UKA’s) has fallen by over 50% to a mere €35 per tonne. The malaise is even more striking when you consider that just across the English Channel, the EU carbon market continues to trade at around €80-85 per tonne.

https://www.ft.com/content/f03d0e82-4527-4a2e-8df8-e744f6238952

https://www.ft.com/content/f893a566-fd17-4915-ad0b-bdd2bd622987, https://www.ft.com/content/4fde34d6-3894-463e-aefe-bc415cadffbb

Other potential talking points include an EU youth mobility scheme and fishing rights.

https://www.betfair.com/exchange/plus/politics/market/1.230583324

The party started in 2018 under the guise of the Brexit Party, but changed their name in 2021.