The carbon abatement return on investment

Emerging markets offer the highest rewards, and China knows it

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below. By subscribing you’ll join more than 5,000 people who already read Carbon Risk. Check out the Carbon Risk backstory and find out what other subscribers are saying.

You can also follow on LinkedIn, Bluesky, and Notes. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

🛫 Note that I’m taking a break from carbon markets next week 🏎️. I will be back at my desk in early July 🛬

Estimated reading time ~ 8 mins

Uncertainty over the future demands from AI and datacentres notwithstanding, energy consumption per person tends to flatten out once incomes reach $25-30k. For many advanced economies reaching this stage, including those in Western Europe and the United States, carbon emissions are also likely to have decoupled from economic growth, or at least begun to do so.

In contrast, as the chart below illustrates, emerging markets (EMs) are on the precipice of entering the ‘energy growth zone’, the steepest part of the S-curve in which rising incomes coincide with a large increase in energy consumption. If these same countries rely on fossil fuels to support the growth in energy demand its clear that carbon emissions will rise sharply. To avoid the risk that fossil fuels become locked in for decades to come, it’s imperative that renewable energy is the foundation upon which future EM energy growth is built.

Low hanging fruit

For climate-orientated investors looking to achieve the biggest cut in carbon emissions per dollar invested, EMs and other developing economies could offer the best return on investment.

The opportunity for additional emission cuts in advanced economies tends to focus on the so-called ‘hard-to-abate’ sectors, all towards the higher end of the marginal abatement cost (MAC) curve. The picture in EMs is very different given the huge low-cost carbon abatement opportunity from renewables and energy efficiency.

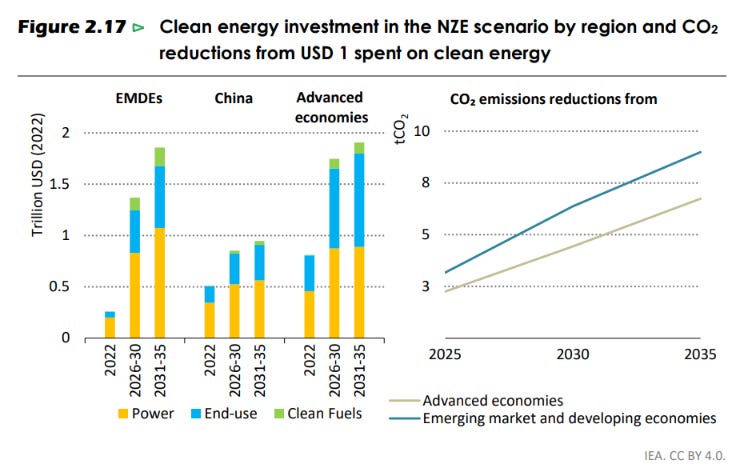

$1 dollar invested in clean energy in EMs could lead to almost 10 tonnes of emission reduction in 2035, according to estimates by the International Energy Agency (IEA) and the International Finance Corporation (IFC), 30% more than the carbon abatement return on investment in advanced economies.1

The opportunity for climate finance is huge. Annual clean energy investments in EMs (excluding China) will need to rise almost 7-fold to $1.4-1.9 trillion by the early 2030s to meet rising energy needs and align with the climate goals set out in the Paris Agreement. The IEA/IFC estimate that around one-third of this investment will need to go into low-carbon generation, another one-third towards energy efficiency and electrification, electricity grids and storage require about a quarter, with clean fuels accounting for less than one-tenth.

Leveraging capital to the EMs

Although EM capital markets are growing, they do not have the depth necessary to meet the widening clean energy investment gap. A substantial mobilisation of global capital flows, primarily from the advanced economies, but also leveraging both public and private sector capital, will be necessary. EM’s dependence on external financing means investors are crucially aware that exchange rate volatility, and political and bureaucratic instability could have an adverse impact on their investments.

In addition to these factors, the cost and availability of finance is a major obstacle to capital investment in EMs. Energy transition investments in particular are typically very capital intensive, requiring significant sunk costs. This means that the absolute and relative cost of capital can make or break the commercial viability of a project. High interest rates could serve to delay the energy transition, especially for EMs and other less developed economies unable to borrow at competitive rates.

The problem of higher capital costs is very real. For example, in developed economies, the benchmark weighted average cost of capital for solar PV projects in 1H 2022 ranged from 1.7-5.8% according to BNEF. In EMs the benchmark ranged from 4.7-14.4%. The broad range tallies with recent estimates from the International Energy Agency (IEA) which estimates that financing renewables costs at least 2-3 times more in EMs than it does in advanced economies.

Carbon credits won’t help, but compliance carbon markets might

For all the talk about carbon credit markets helping to drive investment in the EM energy transition, the data tells a different story. Overall carbon credit value directed at energy projects in EM has increased more than 8-fold over the past decade to almost $300 million in 2024 with Africa the primary beneficiary of these capital flows. However, as the IEA state in the chart below, carbon credit markets have supported less than 0.02% of global clean energy investment, and only around 0.1% of the funds directed at EMs.2

Compliance carbon markets could provide a more bountiful source of capital. Just over half (56%) of the $100 billion in revenue raised from carbon pricing instruments (emissions trading schemes and carbon taxes) was earmarked for energy transition and development projects, the vast majority resulting from funds generated through the sale of EU emission allowances, and all invested in domestic projects in Europe.

Unfortunately compliance carbon markets in EMs are at a much earlier stage of development. Turkey, Indonesia, India, and Brazil, among others are still at an early stage in the development of their own emissions trading schemes. Although these carbon pricing instruments present EM governments with the opportunity to redirect capital towards domestic energy transition projects, the desire to ensure that schemes aren’t too big a burden suggests that the funds invested are unlikely to be a major driver (see Why Asia is pivotal to future carbon market growth).

Advanced nation myopia

EMs are unlikely to get too much help from advanced economies either. EMs are increasingly marginalised as advanced economies focus on the nation-state and their own domestic climate policies. It means that EMs share of future low-carbon investment is only likely to get squeezed even further.

Hopefully it’s not too late before governments recognise that financing clean energy investments in EMs is a positive-sum game. As discussed in A new political trilemma, with EM energy consumption and emissions set to increase sharply, all the hard work being carried out to cut emissions in advanced economies risks being undone:

“Advanced nations should look to invest in less developed countries energy transition and industrial decarbonisation, finance the infrastructure necessary to clean up their environment, incentivise the introduction of policies such as carbon pricing and other regulations, and most importantly, boost trade and investment to help support their economic growth.

This will accelerate their progress through and beyond the tipping point described in the Environmental Kuznets Curve (EKC). This is the point at which economic development reaches a certain level and where further incremental growth results in a decline in environmental degradation, not more.”

China has it’s eye on the prize

The move towards protectionism across many advanced economies, but particularly the United States, has meant that EMs are receiving a greater share of China’s exports of clean technology; 43% in 2024 compared to 24% in 2022, according to recent estimates by BNEF. China has a competitive advantage in solar, wind, and battery technology, and is also eager to find a dependable market for surplus domestic production capacity, one that could be supported through climate finance.

As I discuss in Carbonomics returns: Hydrogen headwinds, a fragmenting world order, and new energy frontiers, China is rapidly developing a competitive advantage across a much broader swath of the technologies necessary for decarbonisation - advanced heating systems to electrify heavy industry, CCUS and industrial carbon recycling, as well as long-duration energy storage systems.

Shutting these technologies out of advanced economies adds to their overall future cost of decarbonisation, but perhaps allows EMs to benefit. Indeed, that already appears to be happening with EMs securing a significant amount of global investment focused on industrial decarbonisation.

A total of 826 commercial scale, clean industrial projects are either operational, at final investment decision (FID) stage, or have been announced, according to the Global Project Tracker from the Mission Impossible Partnership (MIP). If all the projects become operations they are projected to cut emissions by around 1Gt of CO2 per year across the hard-to-abate sectors.3

The 'new industrial sunbelt'

Although China, Europe, and the United States lead the way in terms of investment, one-third of the announced projects are now located in EMs. These new clean industrialisation opportunities are emerging in what MIP calls, “the 'new industrial sunbelt' — regions rich in solar resources, stretching from the Middle East and Africa to Latin America and Asia.4

The best opportunities for carbon abatement are in the EMs; preventing fossil fuels from being locked-in as these economies undergo a dramatic transformation in their fortunes. That will require significant investment in renewable energy, grid modernisation, and clean fuels. Nevertheless, EMs face a challenging funding environment as advanced nations worry about economic and political volatility, and have their attention on domestic issues.

For a country such as China who leads the clean technological race this smells like opportunity. As the West seeks to disengage with China, EMs are also positioning themselves to leverage its industrial decarbonisation technologies, in turn potentially leapfrogging those advanced nations too myopic to recognise the EM carbon abatement opportunity.

👋 If you have your own newsletter on Substack and enjoy my writing, please consider recommending Carbon Risk to help grow this amazing community of readers! Thank You!👍

https://www.ifc.org/content/dam/ifc/doc/2023-delta/scaling-up-private-finance-for-clean-energy-in-edmes-en.pdf

https://iea.blob.core.windows.net/assets/1c136349-1c31-4201-9ed7-1a7d532e4306/WorldEnergyInvestment2025.pdf

https://www.missionpossiblepartnership.org/tracker

https://www.missionpossiblepartnership.org/tracker-insights/jun-25/