It's all political

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below. By subscribing you’ll join more than 5,000 people who already read Carbon Risk. Check out the Carbon Risk backstory and find out what other subscribers are saying.

You can also follow on LinkedIn, Bluesky, and Notes. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 7 mins

“I had always tried to focus on macro, and that had been good for me - but when I look back, I realise how much everything was politically driven.”

- Russell Clark

One of the first pushbacks I get from investors nervous about allocating to carbon markets is the risk of political interference.

Environmental markets such as compliance carbon pricing are a political construction in which scarcity is created through regulation. An emissions trading scheme typically involves the government or another institution imposing a cap on emissions, and then issuing allowances denominated in tonnes of carbon. The emissions cap is then reduced by a fixed percentage each year to move those covered by the scheme towards a long-term target, i.e., net-zero emissions.

Alas, the response from many prospective investors is that well, the rules of the game were set by politicians, and so the rules can also be changed, if and when the whim takes them. A quick step back and you can see that politics is often the driving force behind many of the biggest moves in global asset markets, whether that be commodities, equities, or bonds. The rules of these games are also often rewritten to serve their political masters.

The inspiration to write this post was sparked by a recent article by

, in which the hedge fund manager“I like having a strategy to attack markets with. When you have a strategy, you can makes adjustments to improve it as you get new information. In my career as an analyst and fund manager from 2004 to 2021, I was very heavily macro focused, because that was what worked. But from 2016 onwards, it stopped working. Currency moves, and asset moves that I expected rarely followed through….

...For me, I had always tried to focus on macro, and that had been good for me - but when I look back, I realise how much everything was politically driven.”

In his post, Clark highlights shorting Chinese tech (political impetus to prevent firms getting too powerful), buying Irish bonds at 10% (political will not to see a fellow EU Member State default), as two of his most notable trades where politics was the underlying factor. He goes on to explain what might be behind recent market moves in oil (political pressure to keep prices low in the event of a US or Israeli strike on Iran), and gold (political pressure for higher wages which could fuel inflation, noting the comparisons with the 1970’s) as evidence that politics drives markets.1

You just need to know where to look.

Politics is the driving force in both short-term and long-term moves in asset markets. Trump’s tantrums with Europe or Elon and the risk-off sentiment across asset classes on the one hand. Globalisation, de-unionisation, and the decade long bull market in bonds on the other. Politicians also have their tools of market manipulation. From the US government selling crude from the Strategic Petroleum Reserve (SPR) to keep oil prices low, to the Chinese plunge protection team, buying equites to push share prices higher.

Carbon markets are no different.

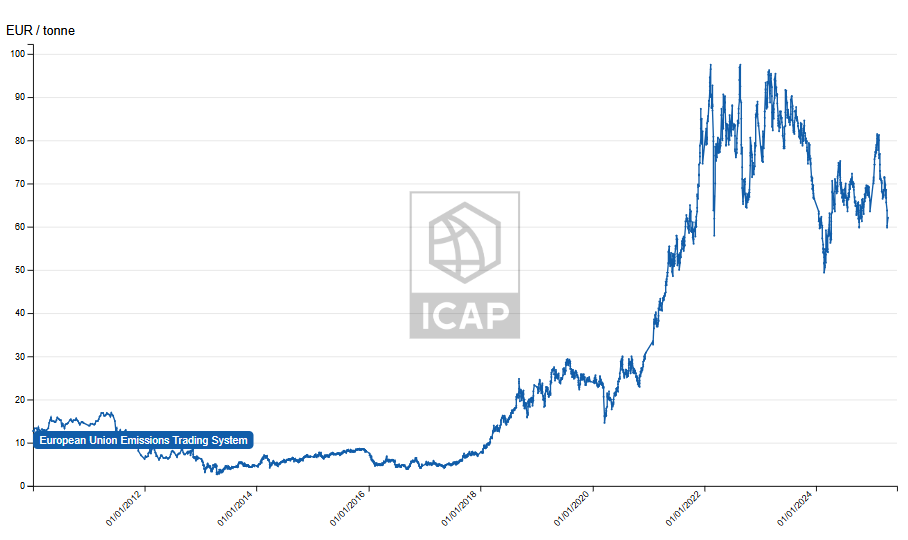

As the cornerstone to achieving Europe’s climate targets, a strong EU carbon market was essential. However, in the early 2010’s Europe faced a problem. Launched in 2005, an influx of cheap international credits had weakened the EU ETS; the price of carbon plunged to below €5 per tonne CO2. The politics of nuclear power generation contributed to the selloff. Japan’s retreat from its climate targets following the Fukushima nuclear accident of 2011 added to the surplus as the government stopped buying credits.

Spurred on against the backdrop of the 2015 Paris Agreement, Europe’s climate policymakers were about to get serious about reform.