Down to earth

Putting a value on biodiversity has consequences, and not all good

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below. By subscribing you’ll join more than 5,000 people who already read Carbon Risk. Check out the Carbon Risk backstory and find out what other subscribers are saying.

You can also follow on LinkedIn, Bluesky, and Notes. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 9 mins

Today is International Biodiversity Day.

The Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES), the inter-governmental body of the United Nations, set up in 2012 to serve a similar role as the IPCC, defines biodiversity as follows:

“The variability among living organisms from all sources including terrestrial, marine and other aquatic ecosystems and the ecological complexes of which they are a part; this includes diversity within species, between species and of ecosystems.”

It finds that biodiversity has been declining at a rate of 2-6% per decade over the past 30-50 years, with half of the global population living in areas experiencing the steepest declines in biodiversity. If these trends are allowed to continue, the IPBES conclude, then it will result in “substantial negative outcomes for biodiversity, water availability and quality, food security and human health, while exacerbating climate change.”

In late 2024, the IPBES published a report described as the “most ambitious scientific assessment ever undertaken” to understand the links between five separate crises or “nexus elements” – biodiversity, water, food, health and climate change. The report estimates that the unaccounted-for costs reflecting impacts on the five nexus elements, are at least $10-25 trillion per year.1

State subsidies such as those that support unsustainable food production practices, have a negative impact on biodiversity estimated to be in the region of $1.7 trillion per year. Private sector financial flows that are directly damaging to biodiversity are estimated to be $5.3 trillion per year (see Fuelling controversy: Fossil fuel subsidies act like a negative carbon price).

Analysts at IPBES estimate that public and private investment aimed at improving the status of biodiversity amounts to significantly less than $200 billion per year (~1% of global GDP). An additional $0.3-1 trillion per year is required to fill the biodiversity funding gap, while the other nexus elements are thought to face a funding gap of least $4 trillion per year.

The report calls for urgent action to “transform values and structures and address the dominance of a narrow set of interests within economic and financial systems”, without which it will be very difficult to “enable increased investments for biodiversity and the other nexus elements.”

Biodiversity as an asset class

Up until recently, biodiversity has been something of an afterthought for sustainability orientated investors. The ‘E’ in ESG more salient (read quantifiable) to those seeking to invest in efforts to mitigate the impact. That is slowly starting to change, but a recent announcement by a major financial institution suggests that biodiversity could become an asset class in its own right.

In late January, BlackRock, the world’s largest asset manager ($11.5 trillion in assets under management as of Q1 2025), released a report titled Our approach to engagement on natural capital, officially recognising nature as a factor in its investment approach:2

“We prioritize land use, water and biodiversity for engagement, as appropriate, as they are most likely to be, or become, material to companies in the near future. The interconnectedness of these components contributes to the availability of natural capital on which companies and economies globally depend in order to operate effectively.”

Citing research published by PwC that found 55% of GDP (~$58 trillion) is moderately or highly dependent on nature, the asset manager indicates that financial markets have barely begun pricing this risk into asset prices:

“BlackRock research shows that only a portion of natural capital’s value to the economy is priced into markets today. This analysis suggests asset prices could adjust to better reflect both the risks and opportunities linked to natural capital, driven in large part by increasing physical risks.”

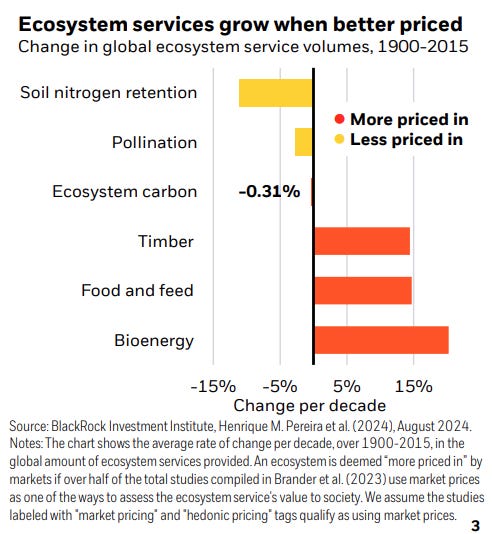

Markets are relatively efficient at attributing a price to natural resources that can be defined as rival goods. Agricultural land is a rival good because only one farmer can cultivate the same field for the same purpose at any one time. In contrast, markets are much less adept at pricing non-rival natural resources, such as wild bees and other pollinators, where one person’s use doesn’t stop another from benefitting.

BlackRock argues that ecosystem services “whose value is not fully priced into markets” are under increasing strain, and that by putting a value on these ecosystem services we will help to rebalance human activity towards their regeneration. If the asset manager is good on its word then increasing amounts of capital will be re-directed towards undervalued biodiversity assets.

The price of everything and the value of nothing

But as Professor Bill Adams of the University of Cambridge writes in the journal Science, simply because you put a value on nature doesn’t necessarily result in a beneficial outcome for biodiversity, and it can actually make things worse. In a world where everything has a value, the services provided by an ecosystem might be enough to save it today, but perhaps not tomorrow. If biodiversity has a price then it can just as easily be traded for something else.3

It’s important to understand that the relationship between biodiversity, biophysical processes, and the delivery of ecosystem services is intricate and poorly understood. An over-confident focus on those aspects that deliver particular services is likely to have an impact (potentially adversely) on other components of the ecosystem, such as those rare species that are much less understood. Furthermore, managing an ecosystem for particular outcomes (e.g., carbon sequestration, flood protection, fire protection) could end up promoting ecosystems that retain little of their original biodiversity.

Meanwhile, in the same way that the long-term price of agricultural commodities changes over time due to innovation, the value ascribed to ecosystem services will now also be subject to technological change. Adams uses the example of how Mexican free-tailed bats helped to control pests from ravaging America’s cotton fields. The value of this particular ecosystem service to the country’s cotton production fell by 79% between 1990 and 2008 as many farmers began to plant a genetically modified cotton that is toxic to insect pests.

The notion of ecosystem services implies that different components can be separated and individually priced. Yet, as Adams makes clear, different ecosystem services are often co-produced. In some cases more of one service might mean more of another, or there may be a trade-off, such that more of one ecosystem service means less of another. Changing preferences towards alternative ecosystem services could mean that the value ascribed to the underlying components is volatile, putting their sustainability at risk.

Finally, Adam’s makes the case that estimating the net benefit of an ecosystem is not enough. Many ecosystems are owned by somebody, whether privately or by the state - although there are exceptions, for example, the deep ocean, the atmosphere, and Antarctica. Decisions as to how ‘owned’ ecosystems are managed “tend to reflect the interests of the owners,” and as Adams goes onto highlight, ecosystem services often require other forms of capital (physical, human, and financial), that in turn depends upon their availability to the owner.

Trade-offs across the nexus

BlackRock expects asset prices will adjust to better reflect the risks and opportunities with the primary driver of this trend likely to be increasing physical risks. The asset manager believes that natural resources are increasingly strained, pushing up costs for companies that rely on them. In turn, biodiversity loss is reducing nature’s resilience and productivity in many regions, further driving physical risks, and so on.

The policy response to biodiversity risks is growing too, albeit with some headwinds. For example, the EU’s Deforestation Regulation requires that certain agricultural commodities sold into the EU market are not sourced from deforested areas. However, even here there is push back due to concerns that it is overly burdensome for business. The law will now come into effect on 30th December 2025, one-year later than planned (see Repricing deforestation risk in the wake of Brazil's presidential election).

Tradeable biodiversity credits issued by governments and tied to various compliance schemes are being developed. The corporate sector is also trying to develop schemes along the lines of those present in the voluntary carbon market (VCM). While the former has a value of around $10 billion, the latter is only thought to be around $2 million! 4

The voluntary biodiversity market is unlikely to get much attention from BlackRock. No, the asset manager has its sight set on 1) circular economy solutions, water solutions and other natural capital themes, 2) green bonds focused on natural capital solutions (~$350 billion of outstanding debt), 3) companies poised to gain from avoiding nature-related risks or leaning into opportunities, and 4) technological innovation related to growing food demand and mitigating the impact.

Biodiversity is intrinsically linked to the other four nexus elements referred to by the IPBES. We all need to be aware of the trade-offs, and especially so as capital starts to put a price on biodiversity. For example, biofuels might help reduce emissions, but their production also competes with the needs of other land-uses such as agricultural production and forests (see Frequent fryer: Demand for biofuels made from used cooking oil is soaring, but could there be a sting in the tail?).

Indeed, the most important conclusion from the recent IPBES report is that prioritising objectives for a “single element of the nexus without regard to other elements (i.e., solely for biodiversity, water, food, human health or climate change) will result in trade-offs across the nexus,” making separate efforts to address them “ineffective and counterproductive.” In short, we need to stop considering them as separate issues, and start tackling them together.

👋 If you have your own newsletter on Substack and enjoy my writing, please consider recommending Carbon Risk to help grow this amazing community of readers! Thank You!👍

Natural capital markets: Putting a price on nature

Carbon markets are just the start of a revolution putting a price on nature.

https://www.ipbes.net/nexus/media-release

https://www.blackrock.com/corporate/literature/publication/blk-commentary-engagement-on-natural-capital.pdf

https://www.science.org/doi/10.1126/science.1255997?sid=d245e8c5-438d-419d-9c1a-139cd617f38d