Carbon intensity: The key to an economically sustainable green transition

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 3,000 people who already read Carbon Risk. Check out what other subscribers are saying.

You can also follow my posts on LinkedIn. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents.

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 11 mins

Carbon intensity is a measure of CO2 and other greenhouse gas (GHG) emissions involved in a unit of activity.

Carbon intensity can be used as a metric at the individual commodity level (e.g., emissions involved in producing or extracting thermal coal, crude oil, etc.), and at the manufacturing process or activity (e.g., emissions involved in generating electricity, steel manufacture, personal transportation, etc.). With companies under increasing pressure to account for, and have an impact on emissions across their supply chains, carbon intensity will become the most important metric by which the market judges progress.

However, the most important measure of carbon intensity is the global economy (e.g., emissions per unit of GDP). A high carbon intensity amplifies the effect of economic growth on emissions. It’s only by dramatically reducing carbon intensity that we can continue to see strong improvements in living standards, while at the same time remaining within the carbon budget necessary to achieve the Paris Agreement.

The carbon intensity of the commodity

Although people tend to use a standard carbon intensity to measure the overall emissions associated with a particular activity, the average hides a broad range of carbon emissions. For example, the carbon intensity of crude oil production varies significantly between countries, but even on a local basis, the carbon intensity can also differ dramatically. The chart below from the International Energy Agency (IEA) shows the global range of carbon intensity for crude oil, by production (Scope 1 and 2), by activity, during 2022. Production of the crudes on the far right of the chart are responsible for ~10 times as much carbon per barrel as those on the far left.1

This second chart from S&P Global illustrates the difference in Scope 1 GHG emissions intensity across production hubs in the North Sea (primarily the UK and Norway). Over 60% of crude production from the basin has a carbon intensity of 10 kgs CO2e per barrel or less. However, similar to the variation on a global basis, the most carbon intensive hubs emit 10x or more GHG emissions as the least carbon intensive.

As energy and commodity producers come under pressure to reduce their environmental impact, cutting the carbon intensity of production is a lever that is within their grasp. For example, crude producers in the North Sea could look to electrify their platform using stand-alone or grid-connected renewable energy, and cut methane emissions by repairing pipelines and other aging infrastructure, and halting the practice of unnecessary flaring (see No free lunch: Cutting global methane emissions from oil and gas is more difficult than it seems).

The carbon intensity of the process

Global carbon emissions associated with generating electricity have doubled since 2000 to 12.4 Gt CO2 in 2022, according to Ember. Around 70% of the growth in emissions has been due to urbanisation and industrialisation in China, spurring rapid demand growth for electricity. Countries with the most carbon intensive electricity generation, such as South Africa and Mongolia, are of course heavily reliant on thermal coal.2

Nevertheless, over the same period the carbon intensity of electricity generation declined by 6% to around 425g CO2 per kWh. Ember data reveals that the largest absolute changes in power generation carbon intensity over that period came from Australia, the USA, and the UK as thermal coal generation was pushed out in favour of natural gas, and renewables captured a larger proportion of the generation mix.3

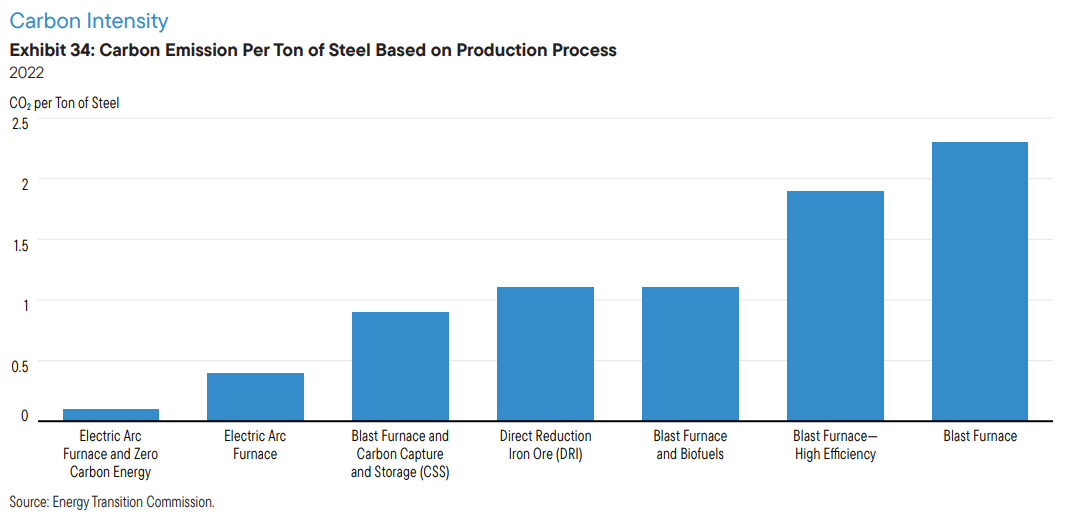

Meanwhile, the steel-production process plays a pivotal role in determining the overall carbon intensity of manufactured steel. Blast furnace operations typically emit 2-2.3 tonnes of CO2 per tonne of steel, while at the other end of the scale, Electric Arc Furnaces (EAFs) typically emit less than 0.5 tonnes of CO2 per tonne of steel. The carbon intensity of the power grid, and the quality of the iron ore used to produce the steel also have an important role to play (see An iron will: Sweden's first mover advantage in green steel will be tough to replicate).

As the chart below illustrates, high carbon intensive steel can push low carbon intensive competition out of the market, especially if they have a cost advantage. Between 2013 and 2022, the carbon intensity of EU steel imports became progressively higher as supplies from China, South Korea, Russia, India, and Ukraine pushed low carbon intensive exporters such as Brazil and Taiwan, out of the market.

The carbon intensity of the economy

Efforts to cut the carbon intensity of individual commodities, manufacturing processes, and other economic activities mean very little if they are counterbalanced by rising carbon intensity elsewhere in the economy. Analysis of 200 years of global emissions and GDP data by the Federal Reserve Bank of San Francisco (FRBSF) reveals that global carbon intensity follows a bell-curve (indicated by the dashed line). Global carbon intensity peaked around 1920 and has gradually dropped to levels consistent with that last seen in the early Industrial Revolution.4

Different parts of the world are of course at different stages of development, yet the evidence indicates that carbon intensity in both advanced and emerging economies do typically follow a similar bell-curve formation. The chart below shows large advanced economies (the US, Japan, and Germany), versus large emerging economies (China, India, and Russia). Advanced economies saw their carbon intensity peak in the 1910’s, while it wasn’t until the 1980’s that emerging economies witnessed peak carbon intensity.

Assuming future carbon intensity is based on countries continuing to follow the bell-curve lower, and combining it with long-term forecasts of real GDP growth by the OECD, the FRBSF projected what it might mean for overall global emissions. Economic, political, and technological factors are inherently unpredictable and so the shaded region broadly reflects the uncertainty (+1 / -1 standard deviation) in the bell curve approach, and the GDP growth projections from the OECD. The horizontal lines correspond to the 2030 emission reduction targets set by the countries of each group in accordance with COP26.

Over the past 30 years, carbon intensity in advanced economies (and to a lesser extent in emerging economies) has diverged (to the upside) from what the bell-curve formation would suggest. This isn’t necessarily something to be concerned about. As the historical data shows, there have been some notable departures from the trend in the past, with carbon intensity subsequently returning to the long-term fitted line of the bell-curve. Nevertheless, FRBSF’s analysis indicates that advanced economies need to play catch-up if they are to return to the bell-curve, and go on to hit their 2030 emission reduction targets. Emerging economies face an even smaller chance of achieving their announced targets, even if they follow the bell-curve. Indeed, the analysis indicates that for this latter group, emissions will still continue to grow and perhaps only peak in 2030 or soon after.

To meet global climate targets, there needs to be much greater focus on bringing carbon intensity at least back into line with the bell-curve trend. As we’ll see, by itself, the market is not doing enough to make this happen, but with government and regulatory support set to ramp up, the chances of success do appear to be on the rise.

Putting a value on carbon intensity

Efforts to differentiate commodities and derived products based on their carbon intensity have, so far at least, proved somewhat illusory. As I outlined in Deciphering nickels green premium, there are three good examples of commodities in Europe where green premiums exist based on low carbon intensity production: aluminium, steel, and ammonia. Each of these commodities benefits from carbon intensity being measurable with a methodology that is agreed upon by industry, while negotiation takes place in an open and transparent market.

If those conditions are in place then the price buyers are willing to pay for low carbon intensity commodities depends on the value they derive from it. Important factors include the potential to reduce emissions at a later stage of production, meeting certain sustainability criteria, differentiating themselves versus their competitors, the size of the carbon benefit, and if it reduces their demand for emission allowances.

The scarcity of the low-carbon commodity relative to the equivalent ‘standard’ emissions substitute is also crucial in determining the existence of a ‘green’ premium. In addition, the existence of additional costs (e.g., the need to procure renewable energy, meet certain criteria) necessary to produce the low carbon commodity - relative to the ‘standard’ emissions substitute - will also influence the size of the premium.

Carbon intensity-based emissions trading schemes

Emissions trading schemes typically operate with an absolute emissions cap. Obligated emitters are required to cut their absolute emissions by an amount equivalent to the annual decline in the cap, or otherwise compete with other operators for an ever scarcer supply of emission allowances.

However, not every ETS operates on this basis. For example, China’s and Australia’s ETS are designed to cut the carbon intensity of obligated emitters to achieve an overall decline in emissions. Under a carbon intensity-based ETS (also known as a tradable performance standard), allowances are allocated according to actual production levels (e.g. kWh of electricity generated) and predetermined carbon intensity benchmarks (e.g. CO2/kWh), either set at the individual plant level or using industry averages. The baseline is adjusted each year to account for changing production levels and the relative and absolute change in carbon intensity by industry.

Under the Chinese ETS, power generators with a carbon intensity higher than the benchmark will have a deficit of emission allowances and must buy allowances to be compliant. While those generators with more efficient plants will show an allowance surplus, which can then be sold to those in deficit. A carbon intensity-based ETS is unlikely to incentivise a shift from coal power to gas or renewable generation. It’s more likely that it will incentivise power generators to switch from lots of old, small, inefficient coal plants towards newer, larger, and more efficient coal facilities (see Everything you need to know about China's national carbon market).

Other carbon intensity-based emission regulations

The EU’s Carbon Border Adjustment Mechanism (CBAM) represents probably the most ambitious and wide-ranging policy tool to incentivise a decrease in carbon intensity. During the CBAM transitional phase - 1st October 2023 to 31st December 2025 - importers must submit a CBAM report every quarter containing information on the quantity of CBAM obligated products imported into the EU, the direct and indirect emissions involved in their production (i.e., Scope 1 and 2 emissions), as well as the carbon price due in the country of production. The cost of complying with CBAM will be gradually phased in between 2026 and 2034. However, significant uncertainty remains as to how importers of CBAM products are going to accurately and consistently report carbon intensity when even the exporters of those commodities might not have access to reliable emissions data (see Through the looking glass: Country level emissions data are (probably) not what they seem).

Governments will increasingly go beyond CO2 and focus on some of the other GHGs. Both the US and the EU are in the process of introducing limits on methane emissions intensity, above which a fee is applied. In August 2022 the US Government announced that it would be introducing a methane fee on its oil and gas industry under the Inflation Reduction Act (IRA). The methane emissions charge began in 2024 at $900 per tonne of methane and is set to rise to $1,200 per tonne next year and $1,500 per tonne thereafter. The "waste emission threshold" above which the Environmental Protection Agency (EPA) will collect the methane fee, ranges from 0.05-0.2%.

Meanwhile, the EU Methane Regulation will impose methane emission intensity limits on imports of fossil fuels into the EU. By 2030 imported fossil fuels will have to meet a maximum methane intensity threshold, or the importer must pay a financial penalty. The methane intensity methodology, the threshold at which a penalty becomes payable, and the financial penalty itself have yet to be decided (see Pricing methane emissions out of the atmosphere: America's first nationwide price on a greenhouse gas does not go far enough).

Remember that we don’t demand energy and other commodities for their own sake, but for what we can do with them. Access to resources has been instrumental in raising global economic development across advanced economies, and they will continue to be vital in improving opportunities for people across the worlds emerging economies.

History shows that global carbon intensity per unit of GDP has peaked and will most likely continue to decline, both in advanced and emerging economies. Recent policy announcements (Europe’s carbon border levy and methane emission limits on the energy sector) are likely to be the first of many such policies that penalise producers with a high carbon intensity.

Carbon intensity is set to become perhaps the most valued metric by which markets judge the competitiveness of different industries, and even the economic prospects of individual countries. A relentless focus on improving carbon intensity is the key to an economically sustainable green transition.

Prosperity bends the curve

"Distinctions must be kept in mind between quantity and quality of growth, between its costs and return, and between the short and the long term. Goals for more growth should specify more growth of what and for what." - Simon Kuznets, the creator of Gross National Product (GNP), the predecessor to GDP.

https://iea.blob.core.windows.net/assets/2f65984e-73ee-40ba-a4d5-bb2e2c94cecb/EmissionsfromOilandGasOperationinNetZeroTransitions.pdf

https://ourworldindata.org/grapher/carbon-intensity-electricity

file:///C:/Users/Peter%20Sainsbury/Downloads/Global-Electricity-Review-2023%20(1).pdf

https://www.frbsf.org/research-and-insights/publications/economic-letter/2023/10/bell-curve-of-global-co2-emission-intensity/

Interesting to see that global emissions intensity peaked so long ago. Who knew? Love the EU steel imports emissions chart by the way, whoever made that is clearly a genius! ;)