Carbon dioxide removal and the buyer of first resort

The window for high cost, novel CDR technologies is closing fast

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 5,000 people who already read Carbon Risk. Check out the Carbon Risk backstory and find out what other subscribers are saying.

⏰ 40% discount off an annual subscription expires on Wednesday 26th February ⏰

You can also follow on LinkedIn, Bluesky, and Notes. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 9 mins

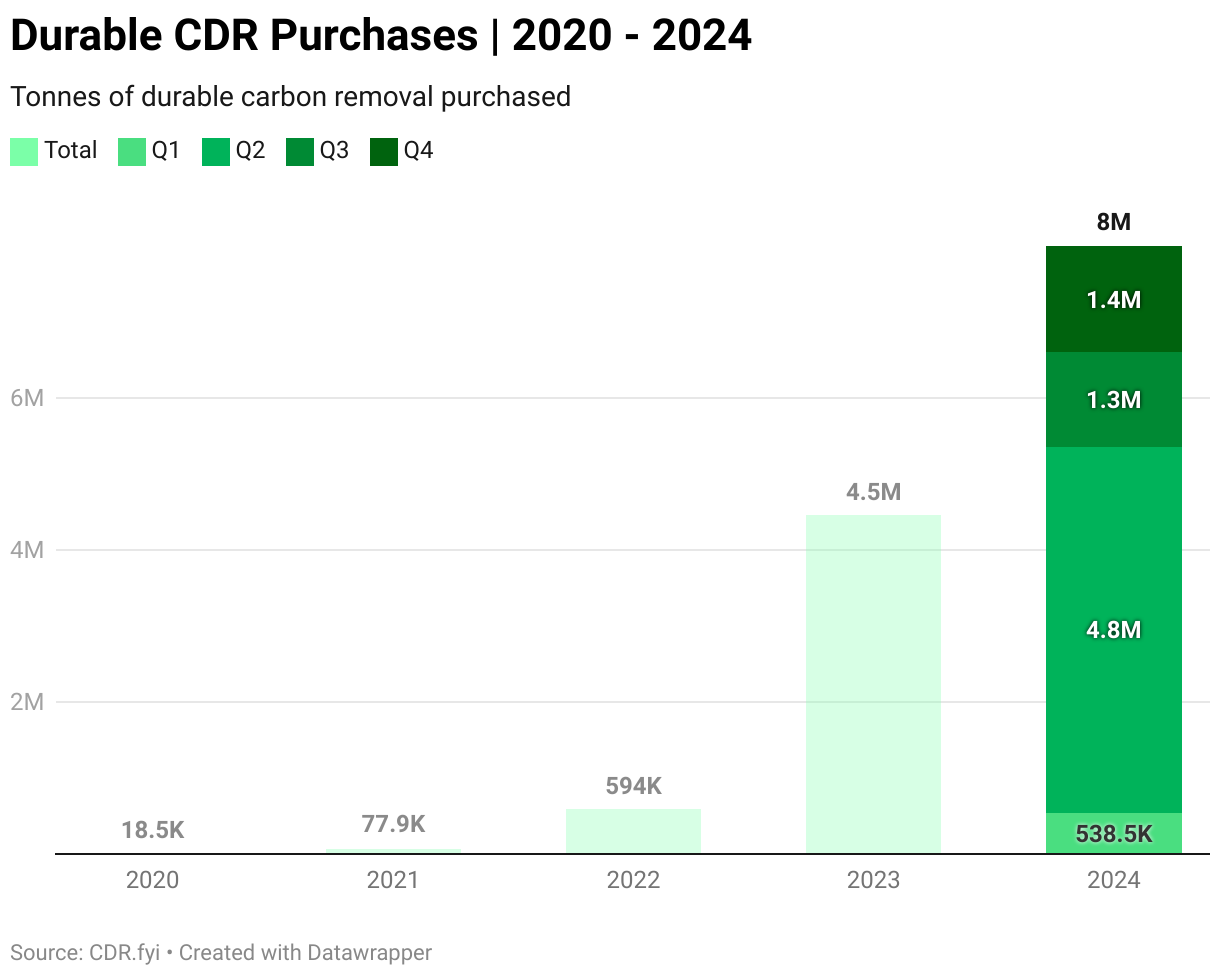

Carbon dioxide removal (CDR) purchases hit 8 Mt CO2 in 2024, according to the latest data from CDR.fyi, an increase of 3.5 Mt CO2 or 78% from 2023 levels. Despite the strong growth, 2024 represents a significant deceleration compared with previous years. In both 2022 and 2023 CDR purchases grew more than 7-fold year-on-year, albeit off a much smaller base.1

The market for CDR purchases is still highly concentrated among tech companies and financial institutions. Their willingness to pay for CDR partly reflects their very high profits per tonne of emissions compared to other industries. Microsoft is by far the largest single purchaser, accounting for 5.1 Mt CO2 or 63% of purchased CDR volume (down from 70% in 2023). In contrast, the share of the market accounted for by new CDR buyers, such as Equinor, the Norwegian state-owned energy company, remains very low at just 9% of purchased volume.

The largest CDR deal of the year was the 10-year 3.3 Mt CO2 offtake agreement between Microsoft and Stockholm Exergi. The energy company runs a biomass plant in the Swedish capital that also supplies heat for district heating systems. Stockholm Exergi will begin construction of a BECCS unit at the plant in 2025, and when its finished it should be able to capture 0.8 Mt of CO2 emissions per year (see The carbon moonshot: Microsoft dominates the market for carbon removal).

As the above example illustrates, the time period between CDR purchases and tonnes delivered (i.e., captured from the atmosphere) is not linear and will vary depending on the technology and where it is in the development process. Nevertheless, it is promising news that CDR removal has been consistently doubling roughly every year since 2020. In 2024, 318.6 kt of CO2 was removed from the atmosphere using technology based CDR (4.4% of CDR purchase volumes), an increase from 145.1 kt of CO2 in 2023. It will need to keep to a punishing growth rate if its to get anywhere near the 10 Gt of annual CDR thought to be required by 2050.

The two lowest cost CDR technologies dominate on both sides of the ledger: tonnes purchased and tonnes delivered. For example, almost 6 in every 10 tonnes of CDR purchased in 2024 went to just two BECCS companies: 41.7% (3.3 Mt CO2) to Stockholm Exergi and 16.7% (1.3 Mt CO2) to Ørsted. Meanwhile, 9 out of every 10 tonnes delivered in 2024 were from companies employing biochar. Note that biochar has accounted for a similar proportion of deliveries throughout the period 2020-2024 (see Nature's 'black gold' rush).

Despite the overall improvement, CDR.fyi believe that “demand is currently insufficient to accommodate the number of CDR suppliers seeking to scale their offerings,” noting that only one-third (36%) of the suppliers listed on CDR.fyi have a registered sale. The problem is that without sales, many CDR start-ups (of which there are now thought to be more than 900), could struggle to raise investment, potentially putting them out of business.2

Many of these start-ups are also developing novel CDR methods, that while typically more expensive than other conventional forms of CDR, could make a huge difference to removing carbon from the atmosphere, if only they were able to achieve economies of scale. For example, while biochar and BECCS CDR credits typically cost $100-$350 per tonne of CO2, other CDR technologies such as DACCS, enhanced weathering, and mineralisation can cost up to $1400-$2,000 per tonne of CO2.

Time may not be on their side. The pool of new CDR buyers isn’t growing fast enough. But perhaps even more concerningly, other research also carried out by CDR-fyi (and in conjunction with OPIS) found that the next wave of CDR buyers is likely to be a lot more price sensitive. This points towards an unwillingness to back relatively costly, novel forms of CDR. Recent announcements by AI heavyweights Microsoft and Meta committing to purchase more nature-based CDR credits, rather than more expensive technology-based CDR, lends credence to the argument that minimising costs is taking centre stage.3

The buyer of first resort

Removing CO2 from the atmosphere is an example of market failure commonly known as the ‘tragedy of the commons’. It occurs when a public resource (also called a commons) is over-exploited as individuals, acting in their own interest, ultimately deplete the resource to the detriment of others. While the cost of removing CO2 is borne privately to whomever pays for it, the benefits accrue to society at large. The upshot is that there isn’t a natural market for CDR. But unless someone is willing to stump up the high costs, technology developers cannot be certain that there will be demand for their CDR service in the future.

Thankfully not everyone thinks that way. There are some companies with the commitment and foresight to make a change.

Back in 2020, executives at Stripe sought to find a way to net out the company’s carbon emissions since it launched one decade earlier. But when they scoured the market, carbon removal companies were few and far between. Stripe’s insight was that rather than invest in supply-side measures (such as giving research grants), it would be far more effective if they could signal that there was demand for CDR, whatever the cost. This demand-side measure is a type of procurement strategy and is a classic way to spur innovation, providing developers with the confidence that a market is guaranteed to exist.

Stripe was the ‘buyer of first resort’.

⏰ 40% discount off an annual subscription expires on Wednesday 26th February ⏰