A uniform global carbon price is unworkable, and unnecessary

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 4,000 people who already read Carbon Risk. Check out what other subscribers are saying.

You can also follow on LinkedIn and Bluesky. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 12 mins

The economist William Nordhaus suggested that the optimal strategy to combat climate change is a uniform global price on carbon:

“The most efficient strategy for slowing or preventing climate change is to impose a universal and internationally harmonized carbon tax levied on the carbon content of fossil fuels.”

The argument for a global price centres on its role as a collective commitment tool, incentivising global participation and cooperation. In facing the same carbon price constraint, so the argument goes, countries would also allocate resources more efficiently.

Capital would more easily be directed at the resources and technology required to decarbonise, in turn reducing the overall global cost of meeting net zero. The prospect of carbon leakage would also be reduced in a world where it was more difficult to undercut your rivals.

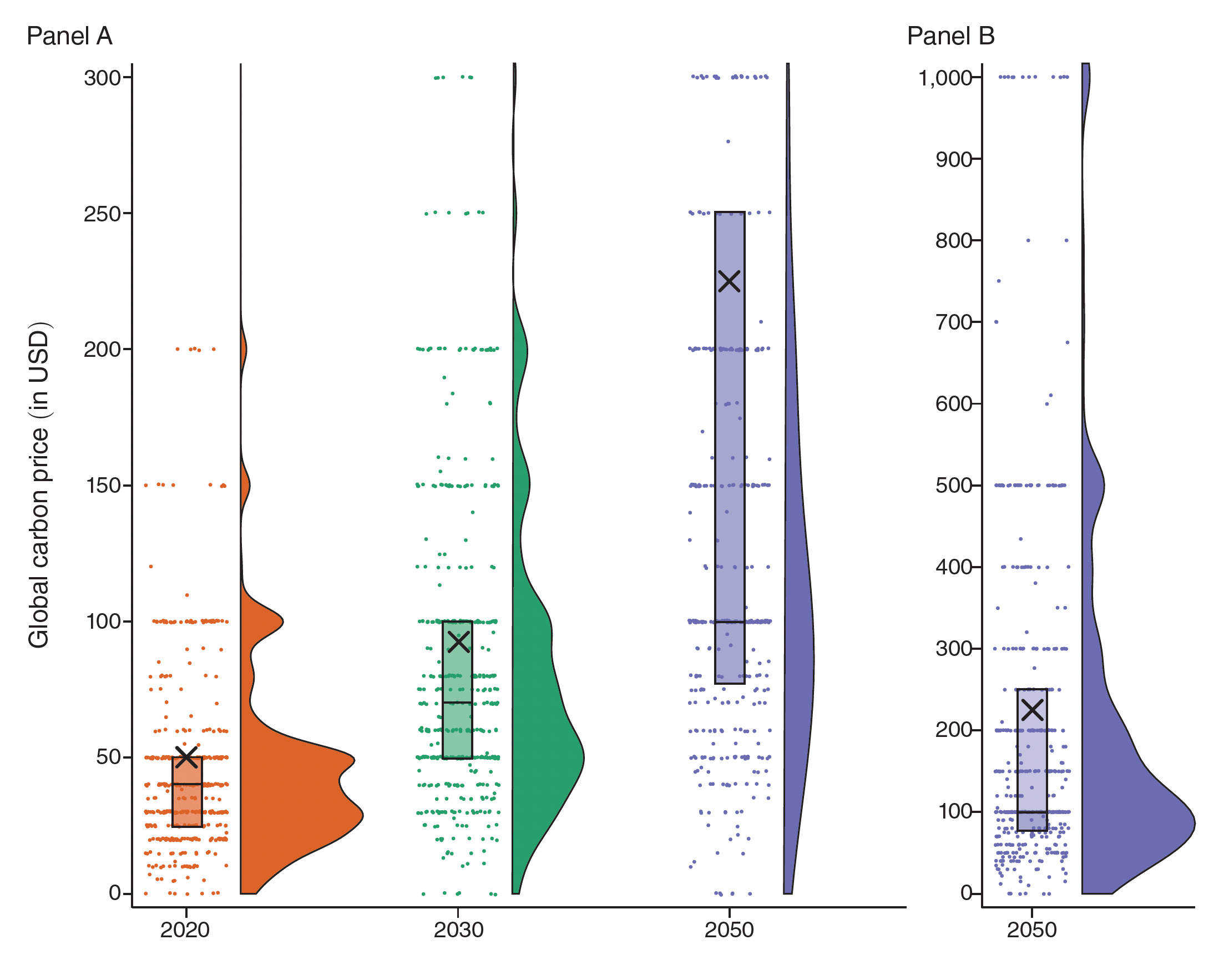

A recent survey of carbon pricing academics asked them to choose a uniform global carbon price, assuming that a “world government” exists and seeks to “maximise the well-being of all present and future people.” Their median response was ~$75 per tonne of CO2 in 2030, rising to $100 per tonne of CO2 in 2050. This broadly tallies with the 2017 High-Level Commission on Carbon Prices (HLCCP), which concluded that carbon prices needed to reach $50-100 per tonne CO2e by 2030, in order to limit global temperature rises to well below 2ºC.1

In reality, a uniform global carbon price is unlikely to be workable. Before we get to some of the reasons why, lets first check in on the status of carbon pricing across the globe to see how far away we are from what the experts suggest.

Note that this isn’t just some academic exercise. It’s going to have real world consequences as exporters of carbon intensive raw materials seek to negate the impact of the EU’s CBAM, or otherwise go to the World Trade Organisation (WTO) arguing their case for a better deal with the EU.

Remember, the CBAM is only payable if the production country-of-origin does not have a comparable carbon price as the EU’s. This effectively pushes countries towards implementing a carbon price at a similar level to Europe. While this helps to coordinate global climate policy and discourage free-riders, it does create inequality (see here and here).

Direct carbon pricing

Almost one-quarter (24%) of global carbon emissions are covered by an emissions trading scheme (ETS) or a carbon tax, according to the latest estimates from the World Bank. Approximately 18% of emissions are covered by an ETS, carbon taxes cover 5.5%, while 0.5% is covered by both an ETS and carbon taxes. Although many emerging economies are looking to introduce or expand the role played by carbon taxes and ETS (e.g., Brazil, China, Turkey, and Indonesia), it is very unlikely that carbon pricing will cover more than 40% of global emissions by 2030 (see It's the carbon price, stupid!).

Only seven carbon pricing instruments, covering less than 1% of global greenhouse gas (GHG) emissions, reached price levels at or above the inflation-adjusted minimum level of $63 (€60) per tonne CO2e in 2024 suggested by the HLCCP. Incidentally, the ETS with the highest price represented in the chart below - the EU ETS - failed to meet even this minimum level, at least in April 2024 when the snapshot of prices for the chart below was taken. Many European countries also have a separate carbon tax - some overlap with the ETS, but most do not - but even these tend to be in the $20-$60 per tonne range.

Emerging economies are at the extreme edges of the carbon price chart. At $167 per tonne of CO2e, Uruguay has the highest carbon tax in the world, albeit it only covers 5-10% of its emissions. With the exception of the South American nation, the next emerging economy on the list is Mexico, where the city of Queretaro has a carbon tax of $37 per tonne of CO2e, 22nd in the rankings of carbon price levels. Of the other emerging economies represented in the chart below, few if any have a carbon price above $10 per tonne of CO2e.

The Effective Carbon Rate (ECR)

Most analysts stop there and only focus on direct carbon pricing policies such as ETS and carbon taxes. But to end here and just compare countries based on their direct carbon pricing would be a mistake.

There are a two other ways that governments typically put a price on carbon: fuel excise taxes and fossil fuel subsidies. Both tip the relative price of carbon intensive products via an implicit price on carbon - both positive and negative. The net average Effective Carbon Rate (ECR) is a way to aggregate the overall impact of these policies into a single price (see Fuelling controversy: Fossil fuel subsidies act like a negative carbon price).

A recent report from the Organisation for Economic Co-operation and Development (OECD) tracks how explicit and implicit carbon pricing has evolved between 2021 and 2023 across 78 countries, covering approximately 82% of global GHG emissions. The tax rates reflect those applicable on 1st April 2023, while ETS’ implemented throughout 2023 are also included.2

Approximately 42% of GHG emissions across the 78 countries covered by the report are subject to a positive net ECR. The average net ECR among the 78 countries was estimated to be €14 ($15) per tonne of CO2e in 2023, down from €17.9 per tonne of CO2e in 2021. Implicit carbon pricing in the form of fuel excise duties remains the strongest price signal across the majority of the 79 countries. The highest ECR in 2023 was almost €160 per tonne of CO2e in Switzerland, the ECR for Germany was close to €90 per tonne of CO2e, while the ECR in the United States was less than €20 per tonne of CO2e.

To complete the picture lets end with data from the World Bank. Their analysts have developed a top-down approach, based on IMF data, to infer the existence of a global net carbon price. Unlike the OECD’s ECR country by country approach, the World Bank’s methodology also takes account of value-added tax (VAT) differentials, and seeks to represent all countries, not just the 78 that the OECD focuses on. Overall, they estimate that the global total carbon price during 2015-23 has typically been in the range of $30-$35 per tonne of CO2.

The capacity of the state

I’ve argued in the past that the perception of a governments commitment to its climate policies is one of the most important factors affecting the price of carbon, especially for an ETS. ‘Political will’ matters, but it’s clearly not the whole story, especially when comparing the price of carbon between two or more different jurisdictions.

A recent paper argues that we should pay much more attention to the states capacity, particularly in terms of its institutions and its fiscal policy. There are basically two types of policy, sticks (e.g., taxes, mandates, cap-and-trade), and carrots (e.g. subsidies, tax credits, grants). Meckling & Benkler argue that “Institutional capacity shapes countries’ ability to adopt and enforce policy sticks, while fiscal space constrains their ability to finance policy carrots.”3

The European Union is very much in the top right quadrant. It uses sticks (the EU ETS, emission standards, renewable energy targets, and coal-fired generation phaseout deadlines), but it also uses carrots (e.g. green hydrogen subsidies). As the paper argues, the European Commission (EC) has “high levels of bureaucratic autonomy in environmental policymaking, allowing it to set the pace for the adoption of climate policy sticks,” but its ability to provide carrots, is more limited given electoral and financial constraints.

The United States (and to a lesser extent Australia, Canada, Japan, and the UK) are in the top left quadrant. This second group of countries “has robust fiscal capacity but limited institutions that support regulatory sticks, and thus may focus primarily on carrots.” US climate policy has typically relied upon subsidies, something that was taken to a whole new level under the Inflation Reduction Act (IRA). Although even here there are limits to fiscal policy (see The net zero fiscal trilemma).

California is located in the lower right quadrant. As a subnational entity, the state has limited tax authority, necessitating a regulatory approach that includes “an economy-wide pricing scheme, a renewable portfolio mandate, the Zero Emission Vehicle mandate, and an energy storage mandate.” Furthermore, the California Air Resources Board (CARB) is “a technocratic and relatively autonomous agency”, and is the key institution “enabling the adoption of climate policy sticks.”

The final quadrant - down in the lower left - includes developing countries that have neither the institutional or fiscal capacity to implement sticks or carrots. The type of climate policy implemented by these countries includes energy efficiency measures - low cost, and come with potentially big benefits.

Nevertheless, a reliance on sticks is likely to necessitate a higher carbon price (or stricter standards and targets) to achieve a desired emission reduction outcome, than would otherwise be the case, if there was a combination of carrot and stick in use. Meanwhile, for a jurisdiction such as California that is reliant on sticks it is the strength (and sequencing) of the non-carbon pricing policies that affect the carbon price required to meet the emission reduction targets (see MAC curve steepening: What California's mix of carbon policies means for price discovery).

The marginal abatement cost (MAC)

Armed with those institutional and fiscal levers in mind, the next factor that affects the relative ECR between countries is the marginal abatement cost (MAC). Remember the MAC refers to the cost of abating the last tonne of CO2 required to meet an emission reduction target. Sloping upwards from left to right, the MAC curve gradually steepens as additional tonnes of carbon emissions get increasingly more difficult, and hence more costly, to abate (see Carbonomics 2023: Chinese EV battery deflation offsets offshore wind cost inflation).

There isn’t just one MAC curve. The MAC differs by country, sector of the economy, company, and by individual point source. It is affected by the cost of inputs including the cost of land and labour, the prevailing interest rate, and the price of energy and raw materials, all of which can very significantly from one country to another.

The composition of power generation assets available is important. For example, if a country relies on hydroelectric power generation (e.g., Brazil) then there is less need for a high carbon price. On the other hand, if a country is heavily reliant on thermal coal generation (e.g. Poland or Japan) then it may need a high carbon price to incentivise a switch to gas generation.

The MAC can also refer to the cost of abating other negative externalities such as air pollution and congestion, while also paying for public goods such as the road network. For example, fuel excise duties are typically used to cover these costs that would otherwise go un-priced by the user.

The higher the fuel excise duty, the greater the incentive to cut back on consumption, or switch to a cheaper alternative (e.g., public transport or a more energy efficient vehicle). Fossil-fuel subsidies work in the opposite, encouraging greater consumption, and discouraging switching towards alternatives.

However, the harder it is to switch - whether to generate power using natural gas, or to ditch the gas-guzzler in favour of an alternative vehicle - the higher the carbon price or fuel excise duty can go before it prompts a change in behaviour. In economics speak demand is highly price inelastic.

The social cost of carbon

The abatement cost is one thing, but there’s also the broader social costs and benefits to consider, and these vary considerably by country. Individual countries acting in their own self-interest, may decide to increase the ECR if they believe the benefits from doing so (in terms of a diminished adverse impact from climate change), outweigh the costs (such as the additional costs borne by domestic carbon intensive emitters).

This is where the social cost of carbon (SCC) comes in. To recap, the SCC is an estimate of the net economic damage resulting from an incremental tonne of carbon dioxide (CO2) released into the atmosphere. It is used by governments to decide whether it is worthwhile introducing a particular environmental policy, such as a fuel excise duty, or EV mandate. As I’ve outlined before though, calculating the SCC is fraught with difficulty, and has the potential to be highly politicised (see Pricing carbon at its social cost: Carbon markets will increasingly be influenced by the social cost of carbon).

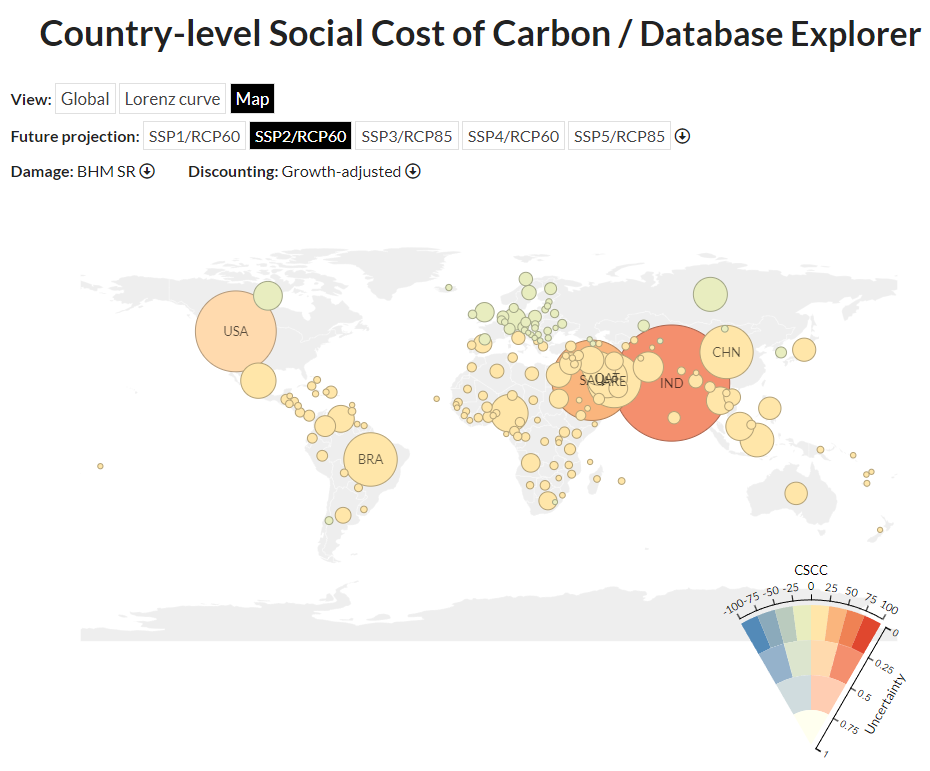

The analysis presented in the map below is based on country-level contributions to the SCC using climate model projections, empirical climate-driven economic damage estimations, and socio-economic projections. The baseline scenarios gives a median global SCC of $417 per tonne of CO2 (with a potential range of between $177 and 805 per tonne of CO2) and a country-level SCC that is unequally distributed. The countries that incur the largest proportion of the global SCC across all scenarios include India, China, Saudi Arabia and the United States.4

It’s the cap, stupid!

A carbon tax involves the government setting a price on the carbon emissions, raising the price of carbon intensive goods relative to lower carbon alternatives. One of the problems with carbon taxes is that the government cannot be sure that the tax is set sufficiently high enough to cut emissions. Even if they can be sure it is the right level today, technological innovation for example might mean it should be set at a very different level tomorrow.

In contrast, an ETS typically involves the government or another institution imposing a cap on emissions. This is achieved through the issue of allowances denominated in tonnes of carbon. The emissions cap is then reduced by a fixed percentage each year to move those covered by the scheme towards a long-term target, i.e., net-zero emissions.

In short, while carbon taxes involves the government controlling the price of carbon and letting the market decide the emissions response, cap-and-trade schemes control for emissions and let the market react by setting the price.

It’s time to ditch the idea that there needs to be a uniform global price on carbon. Being forced to adopt a certain carbon price just because an advanced economy has done so is not efficient. It prevents less developed countries from exploiting their own domestic MAC, while ensuring that the carbon price is misaligned with their SCC. The only sensible path is for each jurisdiction to introduce their own cap-and-trade scheme aligned with net zero.

👋 If you have your own newsletter on Substack and enjoy my writing, please consider recommending Carbon Risk to help grow this amazing community of readers! Thank You!👍

https://www.aeaweb.org/research/charts/pricing-carbon-expert-recommendations

https://www.oecd.org/en/publications/pricing-greenhouse-gas-emissions-2024_b44c74e6-en.html

https://www.nature.com/articles/s41467-024-54221-1#author-information

https://country-level-scc.github.io/explorer/