Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 3,000 people who already read Carbon Risk. Check out what other subscribers are saying.

You can also follow my posts on LinkedIn. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents.

Thanks for reading Carbon Risk and sharing my work! 🔥

* Offer expires Saturday 6th April *

Estimated reading time ~ 11 mins

Every month or so I repost an article from the Carbon Risk archives. The subscriber base for Carbon Risk has grown significantly over the past couple of years and so many of my current readers probably haven’t seen some of the earlier articles. Many of the posts are arguably even more relevant now than the day they were first published. Following that theme, this months repost focuses on carbon credit risk.

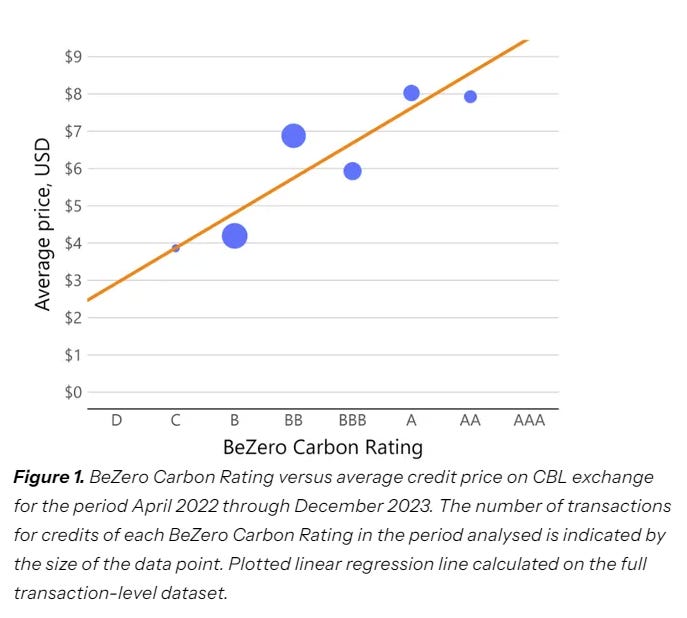

Carbon market innovation never stops, and some of the best ideas can be borrowed from other asset classes. The role that carbon credit ratings agencies are now playing in the carbon credit market is the perfect example. Over the past twelve months the ratings agencies have delivered what the market wants: the ability to price a credit on the likelihood that it will deliver the carbon it says it will. Mirroring the development of the bond market, high quality carbon credits now enjoy a sizeable price premium versus lower quality credits.

The ability to accurately price risk in the carbon credit market, even for projects that have yet to begin issuing any credits, is crucial in boosting investor confidence, and ensuring capital flows to the most promising, most impactful projects. As the scope of credit types assessed expands, and the breath and depth of data available grows, so the efficiency with which risk is assessed and priced will improve. Indeed, there’s evidence that it is already happening. The average price premium for the highest-rated BeZero credits ('A' or above) versus ('BBB' or lower) has surged from around 50% twelve months ago to 200% in late 2023.

At the edge of the carbon market risk curve.

That’s how I described the voluntary carbon market in one of my first Carbon Risk articles.

“At the edge of the carbon market risk curve you will find the voluntary carbon market (VCM).

Up until this point I have only discussed carbon markets from the perspective of the formal carbon compliance markets, such as the ones active in Europe and California.

Regulated. Legal. Transparent. The rules of the market are (mostly) clear.

The voluntary carbon market (VCM) has none of those features.”

The process goes a little like this. A developer seeks to restore a mangrove or reforest a hillside to remove carbon from the atmosphere. A carbon credit can be issued as long as the carbon offset project meets the methodology laid down by the verification body. The decision to issue a carbon credit is a binary answer - yes or no. Once issued, the credits are tagged and tracked, and the holder or purchaser of the carbon credit can surrender it or retire it to meet their carbon neutrality or emission reduction goals, or sell it onto another party.

The developer of a carbon offset project may have passed the verification checks and so be in a position to issue credits, but that does not mean that the carbon project has a 100% chance of success. Carbon offset projects operate in the real world. Their success or failure in avoiding emissions or removing carbon from the atmosphere is subject to significant uncertainty, as is any venture. According to carbon credit ratings agency BeZero, there are six main risk factors that determine whether a carbon credit will deliver on its claims:

Additionality: The risk that a credit purchased and retired does not lead to a tonne of CO2e being avoided or sequestered that would not have otherwise happened.

Over-crediting: The risk that more credits than tonnes of CO2e achieved are issued by a given project due to factors such as unrealistic baseline assumptions.

Non-permanence: The risk that the carbon avoided or removed by the project will not remain so for the time committed and any associated information risk.

Leakage: The risk that emissions avoided or removed by a project are pushed outside the project boundary.

Perverse incentives: The risk that benefits from a project, such as offset revenues, incentivise behaviour that reduces the effectiveness.

Policy: The risk that the policy environment undermines the project’s carbon effectiveness.

The noise

A recent investigation into nature-based credits, jointly published by the Guardian, Die Zeit and SourceMaterial, highlights the challenge faced at the edge of the carbon market risk curve. The researchers analysed the performance of forestry based credits issued under Verra, the largest verification body, concluding that more than 90% of the carbon offsets failed to deliver on the carbon offset claims.1

Of the six risks noted earlier in this article, the researchers highlight risk number 1 - additionality - as the primary reason for the poor quality of the carbon credits. Project developers look to counter this risk by ensuring a reasonable counterfactual or baseline is in place. If the baseline is not estimated correctly then there is likely to be an over-issuance of unjustified carbon credits.

Each carbon project has it’s own unique baseline. Instead, the investigation appears to have applied synthetic baseline, i.e., creating counterfactuals by selecting areas to serve as proxies for the project areas. Sylvera, another carbon credit ratings agency, argues that this approach overestimates the problem. Their own analysis suggests that ~70% of the project baseline estimates could be incorrectly estimated.2

Despite the flaws in its analysis, the Guardian/Die Zeit/SourceMaterial publication has had an immediate impact on the market for reforestation credits (REDD+) with buyers retreating from the market (see ESG investment backlash hits nature-based carbon credit prices).