Ready mixed

How Europe's largest cement producers are rapidly cutting their Scope 1 emissions

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 3,000 people who already read Carbon Risk. Check out what other subscribers are saying.

You can also follow my posts on LinkedIn. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents.

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 12 mins

Europe’s cement industry emits 110 Mt CO2 per annum, accounting for 8.2% of EU ETS verified emissions. Cement comes a close second to the iron and steel industry as the industry with the highest emissions in the EU.

The sector is commonly thought of as one of the ‘hard-to-abate’ industries, and as such it is generally expected to struggle to cut emissions in line with the drop in the EU ETS cap. The upshot is that the cement sector is assumed to need much higher carbon prices to decarbonise.

Unlike other energy intensive industries, there isn’t one single method by which the cement companies can employ to cut their emissions. For example, about 60% of cement emissions in the EU relate to the calcination of limestone into calcium oxide, some 30% of the emissions are due to the need for heat to power thermal processes (it relies on coal for about 18% of its thermal energy); while the rest (~10%) are emissions linked to electricity consumption.

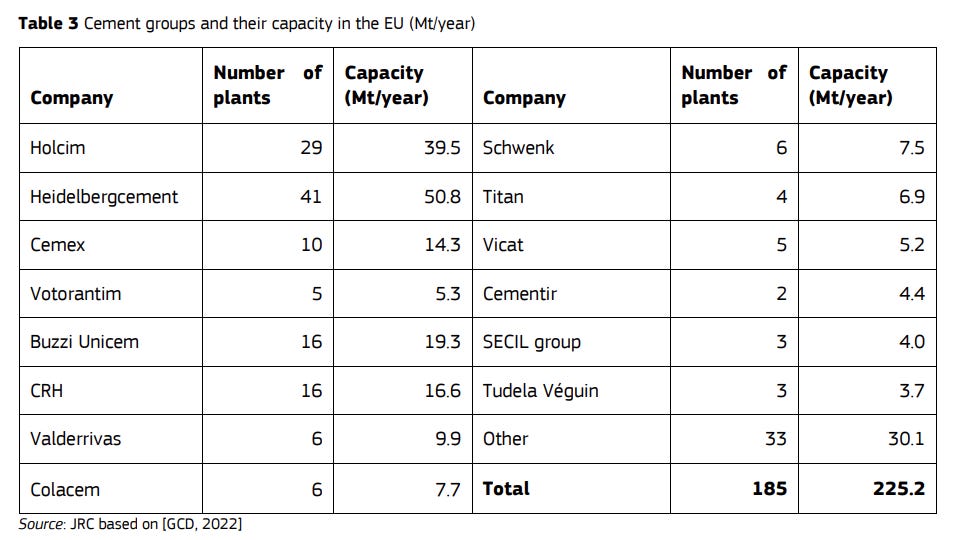

Europe’s cement industry is highly concentrated. Three companies (Heidelberg Materials, Holcim, and CEMEX) accounted for almost half (47%) of EU-27 production capacity in 2022. It means that the actions of just a handful of companies could make a significant difference to one of the most important sources of industrial emissions in Europe.

Up until 2021 the EU carbon price was too low to incentivise investment in decarbonisation. Europe’s cement producers had also been shielded from the full impact of the carbon price due to the high number of free EUAs they had received. The signoff of the EU’s ‘Fit-for-55’ package in 2021, requiring a 55% reduction in carbon emissions by 2030 compared with 1990 levels, changed everything. In addition to the faster emission reduction required, the package also brought forward the phase out of free EUAs.

As the EU’s carbon border levy (the CBAM) is gradually introduced between 2026 and 2034, the proportion of free EUAs available to industrial emitters such as cement companies will also decline. Heidelberg Materials and Holcim quickly updated their emission reduction targets in response to the EU’s more ambitious 2030 climate targets. The cement companies have also spotted an opportunity. If they can cut emissions fast enough they will be able to bank the free EUAs and either sell them immediately, or hold onto them to sell to other industries that might not be able to cut their emissions as easily.

The cement companies are also demonstrating their commitment to decarbonisation in other ways. In late 2022 the Science Based Targets initiative (SBTi), the go-to arbiter of corporate climate action, launched the first framework for companies in the cement sector and other potential users of cement to set near and long-term science-based targets in line with 1.5°C.1

Later that year Holcim became the first cement producer to have its 2050 net zero targets validated by the SBTi under the new framework. In early 2023, the organisation also validated Heidelberg Materials 2030 carbon reduction targets. Other EU cement producers including CRH and Cemex have also received target validation from the SBTi.

Does the EU’s cement sector deserve to be categorised as one of the ‘hardest-to-abate’ industries? Yes, it probably does, but there’s plenty of evidence to suggest its not quite as difficult as many imagine. Lets look at what some of the main European cement companies are doing to cut their emissions.