How to hedge long-term carbon risk

Carbon contracts for difference are the instrument of choice

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 5,000 people who already read Carbon Risk. Check out the Carbon Risk backstory and find out what other subscribers are saying.

You can also follow on LinkedIn, Bluesky, and Notes. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 7 mins

A high carbon price increases the incentive for companies to invest in decarbonisation, but if the carbon price is too volatile it can actually cancel out the incentive to invest. As I discuss in The Fear Index, a 10% increase in carbon price volatility (as measured by the Carbon VIX) has the same detrimental impact on investment as a €12 per tonne decline in the carbon price.

The level of funding required to invest in decarbonising a cement plant, a petrochemical facility, or a blast furnace is enormous, requiring a multi-decade long commitment, and high sunk costs. Exposure to high carbon price volatility makes it much harder for large-scale projects to be seen as ‘bankable’ by investors

Last week the European Commission (EC) announced plans to create an Industrial Decarbonisation Bank (IDB), tasked with mobilising €100 billion over 10 years to support clean manufacturing in Europe. The main instrument the IDB will use to accelerate industrial decarbonisation is an EU-wide carbon contracts for difference (CCfD) scheme.

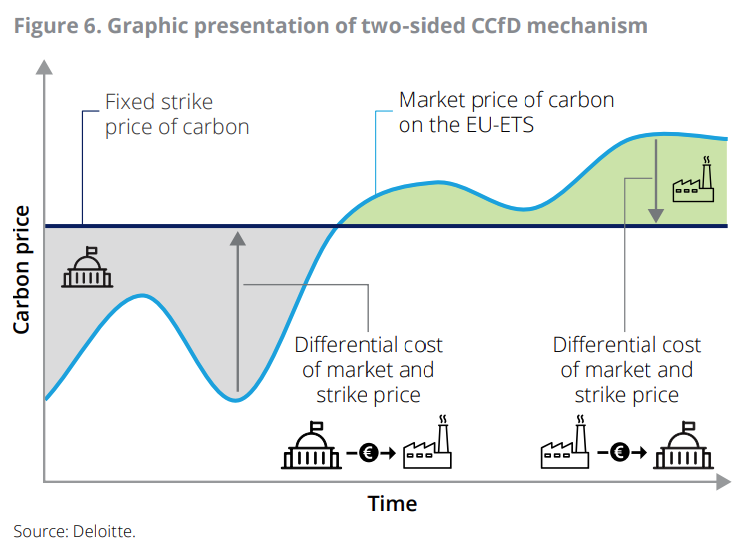

A CCfD works by setting a fixed strike price for CO2. The strike price is normally set at a level that covers the incremental capital and operating cost of the technology. It works something like this. Assume a project developer agrees on a CCfD with the EC at a strike price of €70 per tonne. If at the end of the year the average annual EUA price is €60 per tonne, the EC would pay the developer the difference (i.e. €10 per tonne).

Under a two-sided CCfD, the developer would need to compensate the government if the EUA price rises above €70 per tonne. The alternative is a one-sided CCfD whereby the developer receives a payment if the EUA price falls below the strike price, and gets to keep any excess revenues if it rises above the strike price.

At present futures contracts can only be used to hedge the EUA price up to two or maybe three years ahead. Longer-dated futures contract typically exhibit much lower levels of liquidity, hampering the ability to hedge in size. Without the ability to hedge over a longer period than this, it’s very difficult for project developers to leverage the finance necessary to fund large-scale investments in decarbonisation. CCfDs help correct for this market failure, enabling developers to put a very long-term carbon hedges in place, of around 15 years.

What factors should investors look out for in the design of the CCfD scheme?

Let’s dive in.