Europe's greener cost of capital under threat as monetary policy eases

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 4,000 people who already read Carbon Risk. Check out what other subscribers are saying.

You can also follow on LinkedIn and Bluesky. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

🏆🏭 The deadline for entries to #EUAPredict 2025 is 5PM GMT Friday 10th January. Message Alessandro Vitelli or add a comment to his LinkedIn post with your prediction for the final Dec 2025 EUA contract settlement price 🏆🏭

Estimated reading time ~ 6 mins

The rapid and unexpected increase in interest rates during 2022 was widely thought to be negative for Europe’s energy transition. Isabel Schnabel, member of the European Central Bank (ECB) expressed concern that monetary policy tightening would “discourage efforts to decarbonise our economies rapidly.”

Contrary to conventional wisdom, evidence is coming to light that recent monetary tightening actually helped Europe to decarbonise. According to the European Central Bank (ECB), monetary policy is increasingly transmitted through the economy via a ‘climate-risk-taking-channel’. This acts as a break on the activities of carbon intensive firms, relative to other, less carbon emitting, and emissions intensive parts of the economy (see 'Greenflation' fears are a twin threat to the EUs monetary and climate credibility).

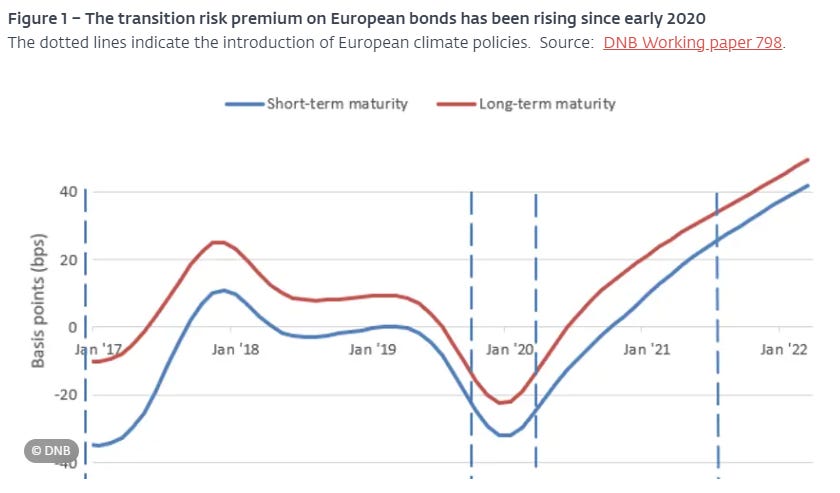

Europe’s most carbon intensive companies pay a premium to borrow compared to firms with lower emissions, according to a report by the Dutch central bank, De Nederlandsche Bank (DNB). The divergence in European corporate bond yields, between high and low carbon intensive firms, has been especially noticeable since 2020 (around the time of the Green Deal and the Fit-for-55 package), with the spread ballooning to over 40 basis points in 2022.1

Importantly, DNB found that the spread in bond yields is evident across both short and long term maturities. The findings imply that companies with lower emissions can finance their operations and invest for the future, at a lower cost than firms responsible for a greater share of Europe's emissions.