A battle for global carbon pricing supremacy is brewing

Why you need to pay more attention to China's carbon market

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 3,000 people who already read Carbon Risk. Check out what other subscribers are saying.

You can also follow my posts on LinkedIn. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents.

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 8 mins

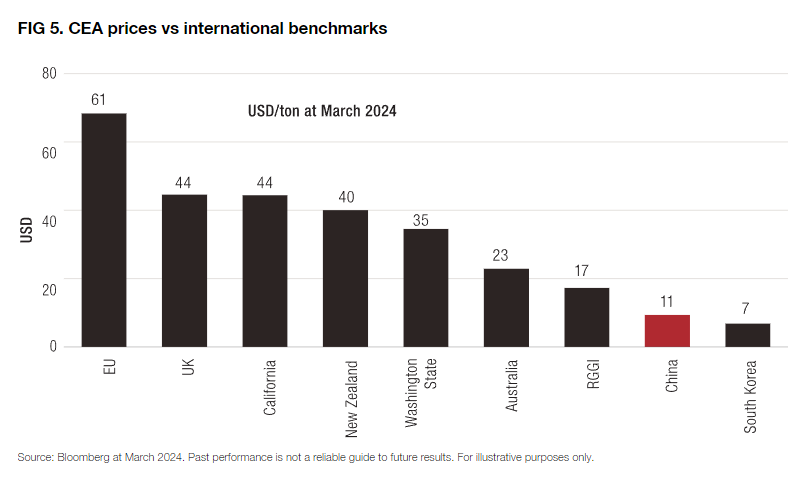

The price of carbon on China’s national emissions trading scheme (ETS) has traded at around €6 per tonne (CNY45) since the market launched in 2021. However, since mid-2023 the China Emission Allowance (CEA) price has doubled as market participants have anticipated a gradual tightening in the market. In spring 2024 CEAs have traded close to €13 ($11, or CNY93.75) per tonne.

It’s good to see the strong performance, but much more needs to be done for China’s carbon price to become a significant driver of decarbonisation. The CEA price would need to rise 4-6 fold to be on a par with more established carbon markets such as the California or EU ETS for example.

Tighter supply and broader industry coverage

As other compliance carbon markets have also found themselves in at a similar stage of development, the Chinese ETS is currently plagued by an oversupply of emission allowances. The London Stock Exchange Group (LSEG) estimates total oversupply at 360 Mt CO2 due to generous carbon intensity benchmarks and dodgy emissions data reporting. In response, China’s Ministry of Ecology and Environment plans to significantly tighten the supply of CEAs.

First, power generation utilities are expected to see the CEAs allocated to them in 2023 subject to a larger than expected retroactive cut. Second, CEAs that have been hoarded and not used for compliance will lose their value after 2025. The latter is thought to account for around 180 Mt, or half of the oversupply in the market. It means that from 2025 onwards only 2025 vintage CEAs can be used for compliance.

China’s ETS currently only covers the power generation sector, mirroring the early development stages taken by other compliance carbon markets. In total some 2,200 utilities, responsible for 4.5 billion tonnes of GHG per year, or 40% of overall emissions are covered by the scheme. Measured in terms of emissions, China’s ETS is already more than 3 times larger than the EU ETS.

Seven other carbon intensive industries (petrochemicals, chemicals, building materials, iron and steel, nonferrous metals, paper, and aviation), are expected to be included over the next few years. Aluminium (both direct and indirect emissions) and cement producers the most likely short-term candidates. If all of these industries join it would mean that around 70% of China’s emissions are covered by its carbon market. At 7.8 Mt CO2, China’s ETS would balloon to 5 times the emissions covered by the EU ETS.

The regulatory framework for China’s ETS allows obligated emitters to cover up to 5% of their compliance obligation with China Certified Emission Reduction certificates (CCERs). CCERs refers to emissions reduction activities conducted by companies on a voluntary basis that are then certified by the Chinese government. Offset projects can include renewable power generation, waste-to-energy as well as forestry (see Everything you need to know about China's national carbon market).

Based on the markets current industry coverage (and assuming participants used the offset option in full) it would equate to 225 Mt CO2 per annum , or 390 Mt CO2 per annum under an expanded industry scheme. It means that China’s ETS has the potential to become by far the largest compliance-based carbon credit market. As Article 6 develops it could put China in pole position to benefit from global demand for credits.

Time to press its advantage

The next twelve months are significant. By early next year countries must submit their next round of Nationally Determined Contributions (NDC), including their 2035 emission reduction targets. One of the key events will be whether Trump returns to the White House in 2025. If he does it could mark another retrenchment in US climate policy momentum. Although that takes the pressure off the Chinese government in some respects, it could be the opportunity for China to press its advantage, and perhaps establish an unassailable lead in global climate policy and delivery (see Climate policy uncertainty is on the rise).

Under an even stronger climate commitment the CEA price is likely to be well supported in the market. DNV has assessed what carbon price is required for China to reach net zero in the late 2040’s. It estimates that China must frontload its ambition and so the CEA price would need to average $100 per tonne by 2030, rising to $200 per tonne by 2040.

China is the worlds largest exporting country and is the biggest trading partner to the EU and the United States. China might recognise that it has an opportunity, in the absence of US resolve to pursue carbon pricing, to become the largest and most important carbon market. China’s ETS could be a counterweight to the EU ETS and eventually supplant the EU ETS as a carbon pricing benchmark used in global trade (see Why Asia is pivotal to future carbon market growth).