Everything you need to know about the Social Cost of Carbon (SCC)

The Social Cost of Carbon (SCC) is an estimate of the net economic damage resulting from the addition of an incremental tonne of carbon dioxide (CO₂) into the atmosphere.

The SCC is often used by policymakers when assessing the cost-benefit impact of climate related policies. For example, the SCC is used in the United States when analysing the impact of vehicle fuel economy standards, power plant regulations, tax credits for carbon capture technologies, carbon taxes, and many more.

Not all countries use the SCC approach. In the UK and the European Union policymakers work back from an agreed upper limit on warming (such as the 2015 Paris Agreement backed a long-term goal of “well below 2°C), setting an emissions pathway consistent with this warming limit, and then determining the carbon price that would be needed to move onto that path.

This “target consistent” approach to weighing different policy options can only really be used in countries or blocs that have an agreed, legally defined emissions reduction target. It’s for that reason that the SCC approach is more commonly used in the United States.

Given the long lead time involved in climate policies the SCC needs to factor in what the world could look like decades into the future. If the SCC estimate is too low then governments may not put adequate support in place to encourage investment and incentivise changes in behaviour. A low SCC may even represent an excuse to rollback climate legislation. If the SCC estimate is too high then economic resources are diverted to combating climate change when they could have been more efficiently employed elsewhere.

It’s important to note that the degree of uncertainty underpinning the SCC assumptions are significant. The SCC must account for the potential impact of global warming on the environment (e.g. agricultural yields, extreme weather, etc.), and uncertainty in the climate’s warming response to carbon dioxide (e.g. climate tipping points).

Although carbon dioxide levels have been gradually building up in the atmosphere, current economic damage from climate change may reflect emissions from several decades ago. In the future a number of tipping points may be reached, such as the melting of giant ice sheets and permafrost and changes in ocean currents. These non-linear impacts are difficult to quantify and make an assessment on their probability.1

The SCC must also consider the long-term outlook for economic growth and changes in population. Both of these factors have a reflexive relationship with the environment and climate change more broadly. Finally, the modelling must use an appropriate discount rate.

Weighing the future

Discount rates are particularly contentious.

People tend to value benefits more when those benefits are received sooner rather than later. This “social time preference” approach reflects the value placed on the future benefits of lower carbon emissions. The discount rate translates the value of the future benefit of climate mitigation into equivalent values experienced today.

The second way of applying a discount rate is that the returns to climate mitigation should be compared against other investments. Everything involves opportunity costs, including mitigating climate change. The upshot of this “social opportunity cost” approach is that the discount rate should reflect the long-term risk free real interest rate.

The third way of calculating the discount rate is one based on ethics. A high discount rate on climate damage implies that the wellbeing of those alive today is worth more than future generations. The geographical inequality of climate change is also relevant as those countries less exposed to climate change are more likely to have alternative investments that can generate a high return and will be less exposed to the negative impacts of climate change. Some analysts suggest that this calls for a very low, or even zero discount rate.

The Stern Review Report on the Economics of Climate Change, published in 2006 and widely considered to be instrumental in moving forward our thinking on valuing climate change, adopted a discount rate of 1.4%, emphasising the ethical approach to weighing the future. Meanwhile, a 2015 survey of almost 200 economists provided a a mean (median) recommended long-term social time preference discount rate of 2.25% (2%). Over 9 out of 10 of the experts were comfortable with the discount rate being between 1% and 3%.

The discount factor can have an outsized impact on the SCC estimate, making or breaking the case for tighter climate regulations and investments in renewables and decarbonisation. For example, under the Trump administration the SCC estimate was a meagre $1-$7 per ton of CO₂.

One of the reasons for the low SCC was the high discount rate assumption. The Trump administration placed a low value on future emission costs by setting the discount rate at 7%, more than double that used by the earlier Obama and subsequent Biden administrations.2

What is the latest SCC estimate?

The US federal government’s current interim estimate of the SCC is $51 per ton of CO₂ and assumes a 3% constant discount rate. However, a landmark 2017 report by the National Academies of Sciences, Engineering, and Medicine (NASEM) pointed out that prior SCC estimates by the US government, up to and including the current interim $51 per ton value, uses dated research and an overly simplistic methodology.

More recent estimates from US federal agencies have moved towards a higher SCC estimate. For example, the cumulative climate related benefits of the Inflation Reduction Act (IRA), recently passed into law in America, could be up to $1.9 trillion, according to estimates from the Office of Management and Budget (OMB). To get to this number OMB estimate the SCC in 2022 to be much higher, around $80 per ton and assumes a lower discount rate of 2.5%.

However, as the OMB report notes, “the interim social cost of carbon estimates are currently significantly underestimated because they do not account for many important climate damage categories, such as ocean acidification, and because of such omitted damages and other limitations and assumptions, these values are likely significant underestimates of the full public benefits of reducing greenhouse gas emissions. These results also do not capture benefits that passing the Inflation Reduction Act will have on other sectors of the economy outside of the impacts that the bill will have on GHG emissions.”

It’s with this backdrop that Resources for the Future (RFF), an independent, non-profit research institution based in Washington, DC. has been working on a comprehensive new SCC estimate since 2017.

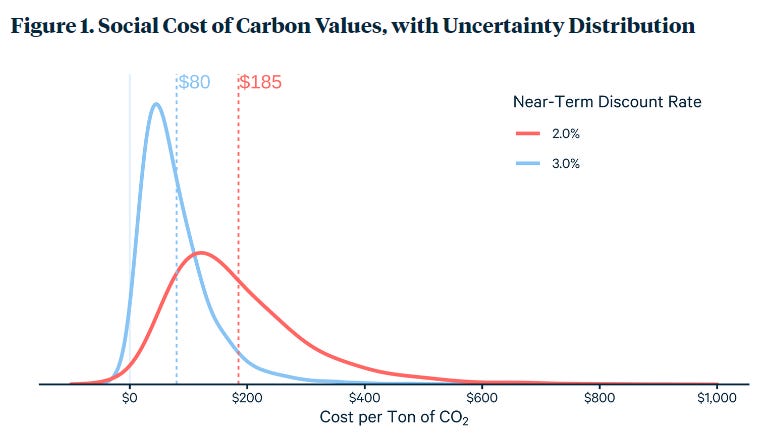

Building on the NASEM report recommendations, RFF recently published an updated SCC estimate in the journal Nature. According to RFF the SCC is $185 per ton, 3.6 times larger than the $51 per ton used by the US federal government, and more than double that used by OMB.

The main reason for the difference is the lower discount rate used by RFF in their analysis. RFF use a discount rate of 2% on the basis that interest rates have declined persistently in the long-run, while also suggesting that lower discount rates are appropriate, particularly for long-lived impacts like climate change.

It’s important to note that the SCC is not a single point estimate. As noted above there are significant uncertainties in modelling the long term economic damage involved with climate change.

Researchers attempt to take account of these uncertainties by using Monte Carlo simulations. The SCC is estimated thousands of times using taking account of the estimated probabilities of the model inputs. The smoothed curves in the chart below reflect the frequency distributions of the SCC estimates made by RFF under different discount rates. The vertical dotted line represents the average, or expected value for the SCC.

According to RFF, dropping the discount rate from 3% to 2% has an outsized effect, more than doubling the SCC estimate. Nonetheless, even absent any change to the discount rate, their analysis still shows a substantial increase in the average SCC (from $51 per ton to $80 per ton), as a result of an updated socioeconomic projection, improved climate model, as well as a better understanding of the damage caused by climate change.

What are the implications of a higher SCC?

Economic theory recommends that an optimal price on CO₂ emissions should be set at a level where the SCC is equal to the marginal cost of emission abatement. In reality, it is impossible for any single government to know where that price should be set. Nor should it. Arguably, it should be left up to the market - within certain boundaries - to uncover that equilibrium price as it will change day by day (see Does a stable carbon market equilibrium exist?).

The updated SCC estimate from RFF suggests that the US government is not placing a high enough value on climate change damage as it should be. This means that vehicle fuel economy standards, power plant regulations and tax credits for renewables need to be much more generous.

Inadequate support for investment and behaviour change risks a situation where climate change impacts go under-priced. The government may then find it is ill-equipped to tackle sooner than expected adverse climate impacts. A climate driven “Minsky Moment” would represent a tipping point from a period of stability, to one of instability, one that forces policymakers into more and more aggressive action (see A climate-driven "Minsky Moment").

Unless the government moves towards a higher SCC estimate (and ramp up government support accordingly), then the implication has to be that carbon prices must move higher do more of the heavy lifting involved in tackling climate change.

https://www.theguardian.com/environment/2022/sep/08/world-on-brink-five-climate-tipping-points-study-finds

The other key reason is that the SCC estimate only considered the domestic costs from climate change. Calculating the SCC based on domestic costs alone would significantly decrease the value, since the majority of the impacts of climate change will not be felt within US borders.