Watch out for €60

It’s often worth looking behind the scenes and trying to unpick how financial participants in the EU carbon market are behaving. Despite claims to the contrary, the actions of financial market participants are an important driver of carbon prices.

In this article I review recent movements in carbon futures positioning and activity in the options market to try to understand what occurred during the August spike in carbon prices, and what it might mean going forward.

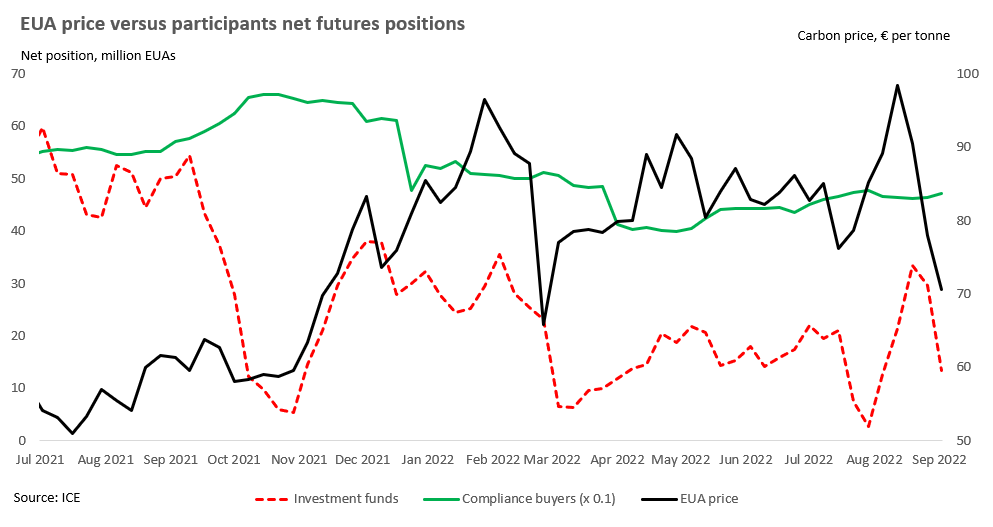

The most closely watched category of trader in the weekly Commitment of Trader (COT) report is IF - investment funds - which encompasses hedge funds and asset managers (see Carbon Commitment Of Traders (COT) 101 at the bottom of this article).

In the immediate aftermath of the Russian invasion of Ukraine, IF’s cut their net length in the market considerably, and then only adding to their net long position gradually. However, by late July net length had reverted right back to levels seen most recently in March 2022, and before that in October 2021. In short, there was plenty of dry powder ready for a renewed assault on the all-time high carbon price.

As power prices went parabolic during August and primary allowance auction supply halved, traders turned to the futures market to hedge the carbon component of their power generation. At the same time investment funds quickly built on their long positions

The fraught margin call situation affecting European energy traders (estimated to be around $1.5 trillion), increased signs of industrial demand destruction and political uncertainty related to the energy and carbon market have accelerated the pull back in prices (see Hibernation: How the EU carbon market is adapting to a long geopolitical winter).1

It’s probably best to think about the August carbon trade as a dramatic short squeeze that has now unwound (see The sword of inelastic supply cuts BOTH ways). The speed of the subsequent decline makes the return to prices below €70 per tonne seem more dramatic than it first appears. Afterall, the carbon price was only around the €75 per tonne level as recently as the last week in July.

Net positioning among investment funds is now back in line with where its been for most of the summer.

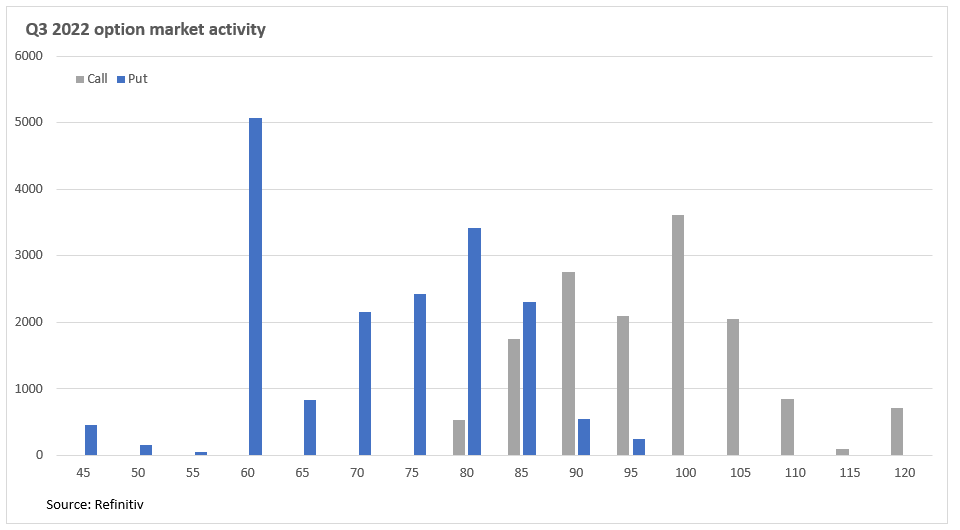

What clues can we learn from the options market? The main area of option contract activity for end Q3 is around the €60 per tonne mark. That could be a target over the next couple of weeks as the September contract nears expiry. An overall put-call ratio of 1.22 is also quite bearish.

Meanwhile, the options market for the Dec-22 futures price, the most heavily traded contract is more balanced. The overall put-call ratio is 0.98. However, as with the Q3 contract there are significant put call volumes around the €60 per tonne mark, but this time there is also large volumes going all the way down to the €30 per tonne level. EUA futures need to rebound to the upper reaches of the 90’s before options market activity really provides a bullish tailwind.

In my most recent article I concluded that the carbon market “remains essential to the bloc meeting its carbon emission reduction targets. I think that we’re more likely in a period of hibernation, one where the EU ETS can preserve and build on its strength, ready for when the bleak winter finally ends.”

The key thing to watch out for over the next couple of weeks is the €60 per tonne level. As I mentioned in the earlier article there has been little public mention of €60 per tonne being an implicit floor for carbon since the German government first raised it when they came to power in November 2021.

Things have clearly moved on since then.

€60 will be a key test of political resolve and the EU’s commitment that the carbon price is ‘The Currency of Decarbonisation’.

Carbon Commitment Of Traders (COT) 101

Positioning analysis allows a carbon trader or longer term investor to understand how market participants behave under different circumstances in the market - fundamental, technical and sentiment. If you can predict behaviour, and be able to correctly anticipate the risk that capital flows will move one way or another, then you have an edge over other traders in the market.

Positioning data is probably the most underutilised tool in commodity markets. It breaks down open interest (the number of open contracts) during a particular period, split between different types of market participants, and according to whether they were long or short. Remember that futures markets are zero-sum - for every buyer of a particular commodity futures contract (a ‘long’ position), there must be a seller on the other side (a ‘short’ position).

Commodity futures exchanges tend to publish data on the hedging and speculative activity of participants on a weekly basis. This publication is known as the Commitment Of Traders (COT) report. The Intercontinental Continental Exchange (ICE) COT reports breaks down futures market participants into the following five categories:

IFCI: Investment firms or credit institutions

IF: Investment funds

OFI: Other financial institutions

CU: Commercial undertakings

Other: Operations with compliance obligations under directive

There are four challenges carbon investors have about using positioning analysis: the time lag between when open interest data is collected and published, how traders are classified, the challenge in disentangling the motivations of traders, and the ‘age’ of the positions.

The ICE typically publishes the COT report on the same day each week. Although there is a small lag in the positioning information, its important to remember that this data is still very much real-time compared with almost all other data that is reported in the market. Importantly, everyone in the market gets the same report, at the same time.

The second concern relates to how traders are classified. For example, simply because a CU and Other are compliance buyers does not preclude them from using commodity futures markets for speculation, in addition to hedging. Meanwhile, some of the activity in the IFCI and OFI category will also involve hedging on behalf of compliance buyers. This muddies the water to some extent in interpreting the motivations of the various participants in the market.

The third challenge that investors raise about positioning data supplied by the COT report is closely related to the second concern above. How to disentangle the motivations of traders? For example, IF’s are a broad church and include macro funds trading equities, a commodity fund speculating on the shape of the futures curve, an index or ETF management firm. This can mean that positions are placed that do not solely reflect participants view on the price direction of carbon.

The ‘age’ of the positions is also a concern. For example, long-term investment positions - for example, positions that underpin carbon ETFs and long-term hedging positions - can make certain positioning profiles difficult to interpret.

Investment fund (IF) behaviour

The most closely watched category of trader is IF - investment funds - which encompasses hedge funds and asset managers. Despite the concerns over categories expressed above, market participants must, in the main, behave according to the category that they have been assigned.

One factor here is crucial, market participants in the IF category have to close out their positions, i.e. they can’t go to delivery. If they are playing in the physical market they would have to have been assigned to a different category. And so when you see a very large short position in the IF category they are going to have to close that position out.

This can get interesting when prices are at an extreme. For example, it can often be a very interesting buying opportunity when you see that money managers have made a nice paper profit by building up a large short position, especially if prices are at the lowest level for some period of time.

In the past week more than 40 CEOs of European metal groups have warned of an “existential threat” to the industry due to high energy prices. According to the letter, "50% of the EU’s aluminium and zinc capacity has already been forced offline due to the power crisis.”