Short covering brings carbon market bulls out of hiding

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 3,000 people who already read Carbon Risk. Check out what other subscribers are saying.

You can also follow my posts on LinkedIn. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents.

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 8 mins

Its been a long bleak winter for EU carbon market bulls.

But for investment funds and other investors able and willing to play the short side, the bear market in carbon has been one wild ride.

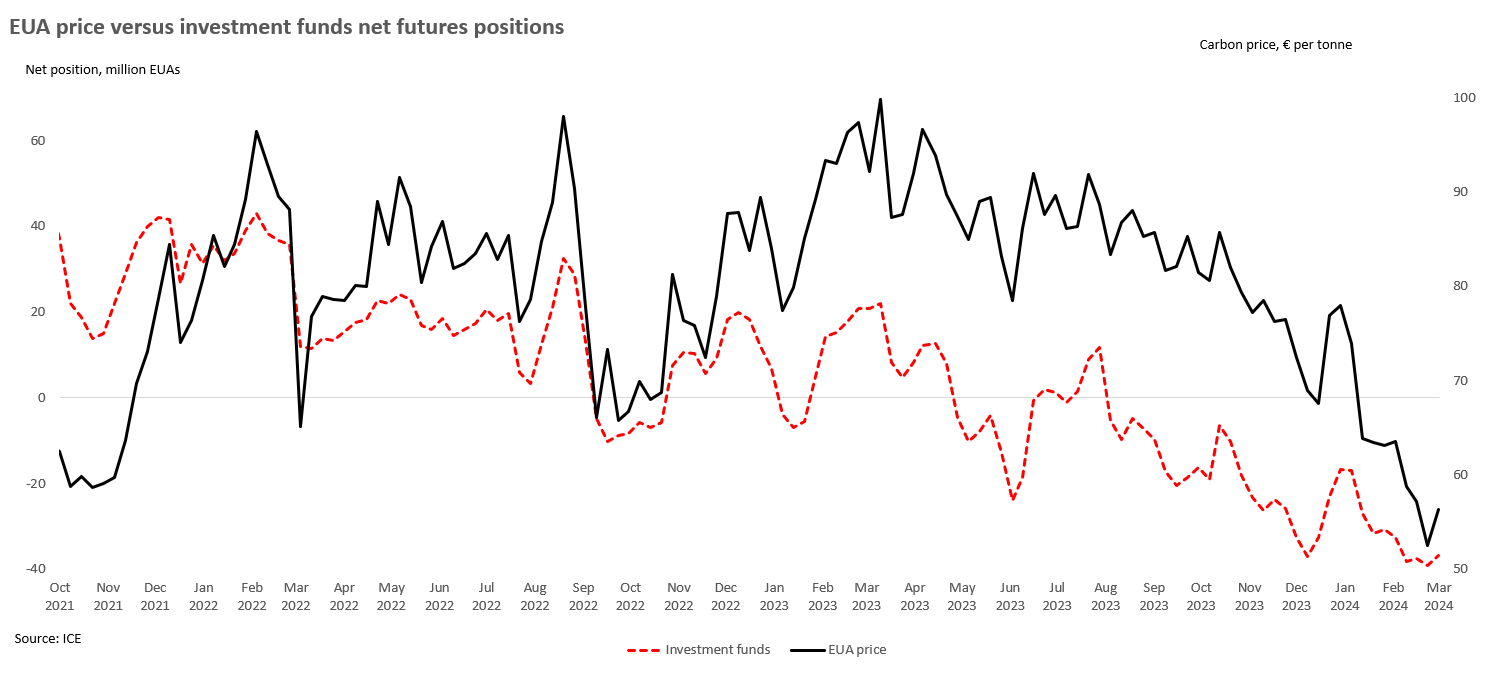

Twelve months ago, with the EU carbon price flirting with €100, investment funds sat on a net long position of almost 22 million EUAs. Funds rapidly trimmed their long positions as the market failed to breach this psychological barrier.

Since August though attention has been firmly focused on the weak fundamentals and positioning has decisively shifted to a net short. Apart from a brief change of direction in late December, the market has been overrun by the bears with every step down in European natural gas prices being an additional reason to build EU carbon short positions (see Deflationary expectations).

Nevertheless, we may be approaching the point that the bulls come out of their winter hiding. The latest COT report (w/e Friday 1st March) shows that investment funds may have begun to close out some of their shorts. After reaching a record 74.6 million EUAs in the previous week, short positions have since been cut by 2.4 million EUA’s. The overall net short position may have fallen slightly to 36.8 million EUAs, but this remains huge by historical standards.

If you are new to carbon futures positioning data then check out the EUA COT 101 explainer at the bottom of this article ⬇️.

The problem with crowded trades is that it only takes a small spark for traders to start running for the exits all at once and seek to cover their shorts. Worries over LNG supplies from the US, and the discovery of corrosion at the Blayais 4 nuclear power plant in France have been sufficient for traders to turn bullish on European power and natural gas markets. Bear market rallies in any asset can be explosive, and that’s exactly what we’ve seen in carbon, as EUA’s surged more than €10 to above €60 (see France's nuclear risk premium has faded, for now).

The options market often acts as a anchor for prices ahead of futures contracts coming up to expiry. It may point to even more upside, at least in the short term. The main area of option contract activity for end Q1 is around the €65 strike, with further significant interest at €80 strike. At 0.79, the overall put-call ratio gives a bullish signal for EU futures prices.

The question is whether upon expiry, the market succumbs to its bearish tendencies once more and looks to retest €50 as a market floor. A crucial level as €50 marked the level where the EU’s ‘Fit for 55’ package was finally approved, and from where the market could begin to set it’s sights on much higher carbon prices.

Speculators always get the blame…

Given the role played by funds in price discovery it’s not surprising that they occasionally get the attention of the regulator. This usually happens towards the top of the market when speculators are often blamed by politicians for ‘forcing’ prices beyond that warranted by the fundamentals. And so it was during the boom in carbon prices during 2021.