Running of the bulls

Investment funds position for higher EUA prices

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 4,000 people who already read Carbon Risk. Check out what other subscribers are saying.

You can also follow on LinkedIn and Bluesky. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 4 mins

Investment funds active in the EU carbon futures market returned to being net long in w/e 15th November; the first time this has occurred since July 2023. The latest Commitment of Traders (COT) report for w/e 22nd November shows that funds have continued to build net length, and now sit on a net position of +9 million EUAs.

The previous net short position reached a peak of 39 million EUAs during late February, around the time that the EUA price hit a low of €50. The most recent contraction in the net short began in mid-October with funds primarily closing out their short positions. However, since the start of November funds have been building up their long positions, perhaps signalling optimism that the EUA price might increase through the rest of the year and into 2025 (see Good green derivatives: A peek beneath the hood of the EU carbon market).

The caveat to this is that it’s unclear whether these are short-term tactical positions, or more longer term bets on a resumption in the EU carbon bull market. If it’s the latter then it’s clear from the chart below that there’s more room for shorts to close out and funds to continue adding to their long positions. For example, in the weeks preceding the Russian invasion of Ukraine, funds held a net position of 43 million EUAs, with a long position of 66 million EUAs.

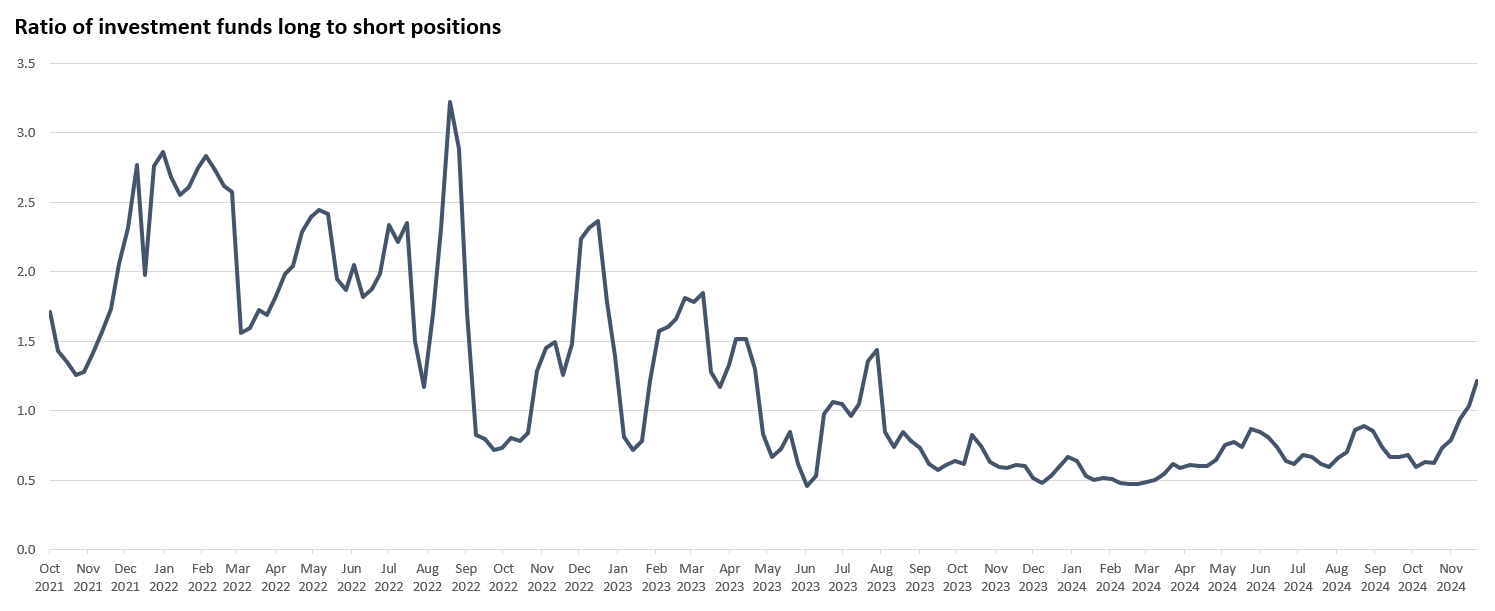

Another factor indicating the potential for upside is the long/short ratio. It’s only in the past week or so that the ratio moved above 1 (i.e., indicating more longs than shorts). The left hand-side of the chart shows there is significant more scope for upside if optimism of a return to the €80-€100 level builds.

Options market activity exhibits a split in opinion as to where carbon prices might finish the year. The main area activity for December is around the €50 and €90 strike price. However, the overall put-call ratio is 0.81 which tends to point towards a bullish outlook for the EUA price into the year end, coupled with significant call activity at the €70 and €75 level which could offer support (see Escaping the Euro doom loop: A new steady state, the power of narrative economics, and the mispricing of consensus expectations).

A key test could be upon us, one that could signal if investment funds are going to be on the long side for longer.

After breaking out of the upper channel (one that’s been in place since early 2023), it looks like the market might be retesting the top of the channel again, checking for support. The 100 and 200 day moving averages (as well as the 23 and 30 day exponential moving averages) are converging on the €67 level and this could also offer strong support at this level. On the other hand, a move below this level might presage a deeper pullback in the carbon price.

Happy Thanksgiving to all my readers from the United States 🦃

👋 If you have your own newsletter on Substack and enjoy my writing, please consider recommending Carbon Risk to help grow this amazing community of readers! Thank You!👍

Hedging your portfolio against carbon price risk

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭