Repost: Is a repeat of 2021 on the cards for California's carbon market?

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access.

By subscribing you’ll join more than 3,000 people who already read Carbon Risk. You can also follow my posts on LinkedIn and benefit from my referral program. Thanks for reading!

Estimated reading time ~ 9 mins

Amidst the general malaise that has afflicted the EU carbon market in recent months, it’s easy to forget that other carbon markets do exist. Indeed, one particular market is setting record highs.

The price of Californian Carbon Allowances (CCA’s) has increased by ~50% over the past twelve months to $42 per tonne (€39). As I outlined in the article below from July last year, the pressure to comply with an upcoming compliance deadline is likely to drive increased demand for allowances. Speculators have pre-empted this move of course, but the bullish backdrop has also been supported by low offset issuance and strong signs of policy commitment from the state.

It’s worth remembering that there are mechanisms in place that could be activated in the event that CCA prices increase further. For example, two cost containment reserve tiers are set at $56.20 per tonne and $72.21 per tonne enabling additional supply to enter the market. Meanwhile the price ceiling is set at $88.20 per tonne (see An asymmetric bet on a phase transition).

With CCA prices potentially set to increase further into the compliance window and EUA prices continuing to fade, the chances that the Californian market trades at a premium to the EU ETS later this year are growing. That would represent a remarkable turnaround for the Californian market, after many years in Europe’s shadow.

A major compliance deadline in the California carbon market is approaching in November 2024. The race to secure sufficient emission allowances could spark the next big upward move in the state’s carbon price.

Normal procedure requires obligated entities to surrender Californian Carbon Allowances (CCA’s) equal to 30% of the previous year’s verified emissions by the start of November. However, CCA’s equal to all remaining emissions must be surrendered by November in the year following the last year of a compliance period.

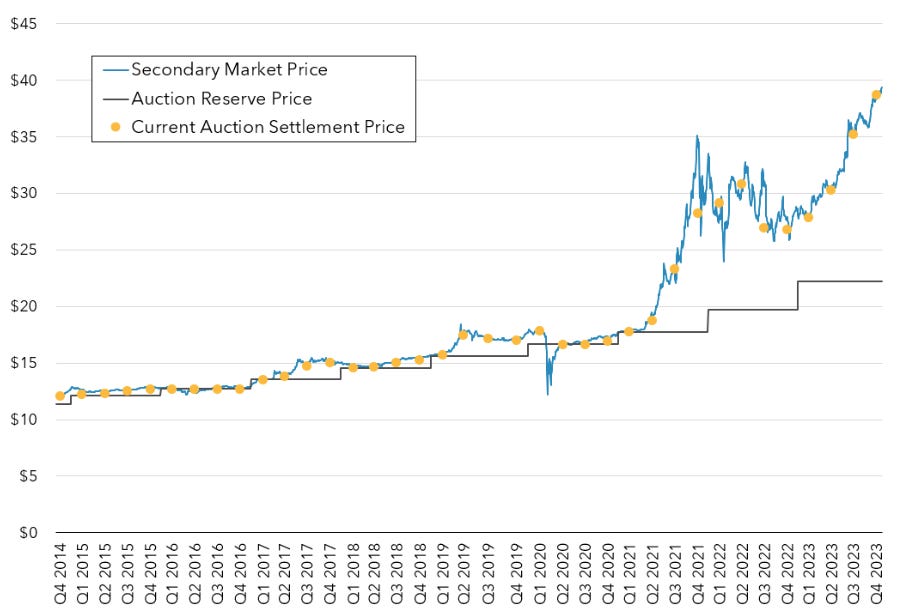

California’s carbon market is now in its fourth compliance period (2021-23), which means that obligated entities must deliver sufficient CCA’s to cover the entire compliance period (minus those already delivered) by 1st November 2024. The last time this happened was of course in November 2021, at the end of the third compliance period (2018-2020).

Back then demand at the previous quarterly auction (Q3 2021) was especially strong, clearing at what was then a record 32% premium above the Auction Reserve Price (ARP). An influx of investment fund activity was partly responsible for the surge in demand. Around 30% of the auction volume was sold to investment funds, anticipating that the compliance window was nearing. In response, the CCA futures price jumped from ~$18 per tonne in early 2021 to a high of $35 per tonne in early November. 1