Pipe dreams

The United States is set to become a carbon capture superpower later this decade, but it will need a massive expansion in its CO2 pipeline infrastructure if it is to reach its full strength.

The US is crisscrossed by ~4.2 million kms of pipelines, predominantly funnelling trillions of cubic feet of natural gas each year, as well as hundreds of billions of tonnes of liquid petroleum products.

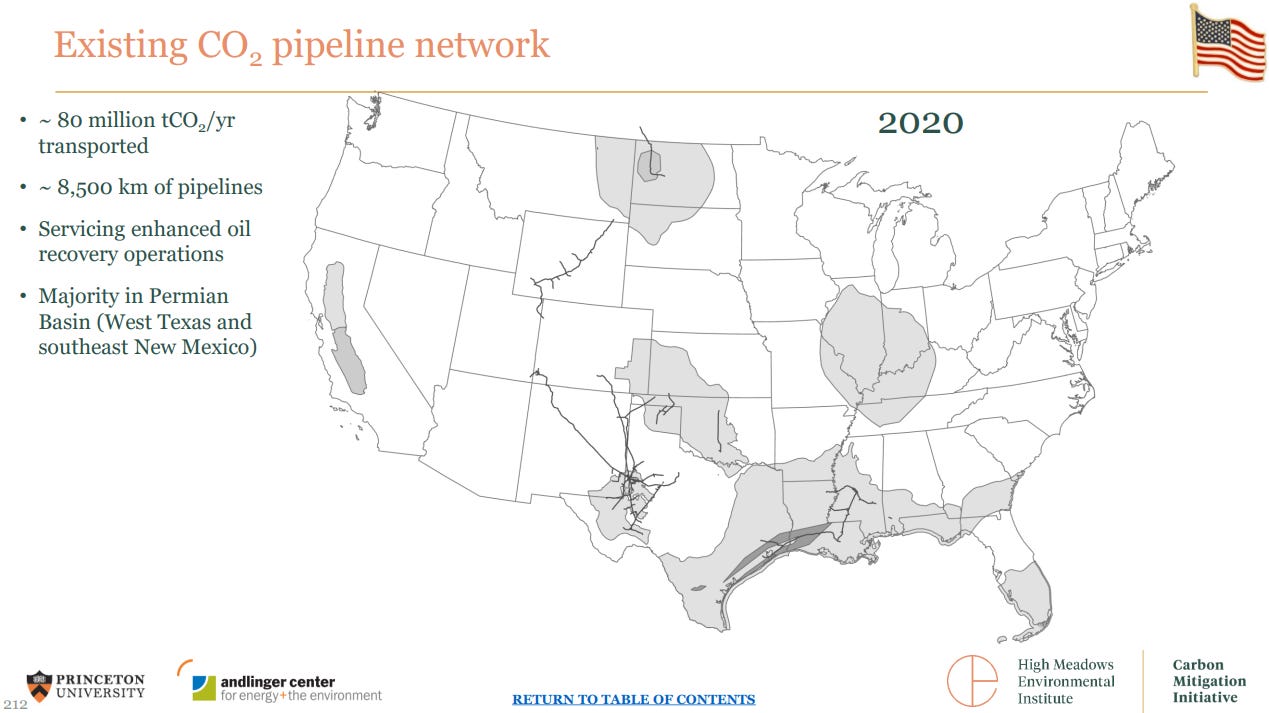

In comparison, the length of pipelines dedicated to transporting carbon dioxide (CO2) are miniscule in comparison. In the US there is estimated to be ~8,500 kms of CO2 pipelines, primarily located in the Permian Basin, Texas. The nations CO2 pipelines currently transport 80 Mt CO2 each year, with the majority of the CO2 being used for enhanced oil recovery (EOR).

Pipelines are usually the cheapest way to transport CO2, especially when transporting large volumes. Transporting CO2 by onshore pipeline is estimated to cost ~$6 per tonne CO2 per km, while offshore pipelines cost ~$10 per tonne CO2 per km. Trucks and rail compete with onshore pipelines are more expensive but offer flexibility for the last mile, whereas ships can only really compete with pipelines once the distance travelled is greater than 800km.1

Analysis from BNEF published last summer forecast that US carbon capture capacity (including emissions captured from power, industry and Direct Air Capture) will soar from some 20 Mt CO2 today, to 134 Mt CO2 by 2030 based on likely projects already announced (see The carbon capture superpower: The United States will dominate global CCUS capacity). However, their projection did not take into account the likelihood for a bounce in capacity announcements following the announcements in the US Inflation Reduction Act (IRA).

Other analysts were much more aggressive in their outlooks. For example, Rhodium Group projects that US carbon capture capacity will reach ~100 Mt CO2 in 2030, but could rise to ~300 Mt CO2 by 2035 as new capacity comes onstream. A separate analysis by researchers at Princeton University thinks carbon capture could grow much faster, rising to ~200 Mt CO2 in 2030 and to 450 Mt CO2 in 2035.

With the country’s carbon capture capacity projected to rise at least six-fold by the end of the decade, and perhaps as much as 40-fold by 2035, there is a pressing need to build out the country’s network of CO2 pipelines. With no means of transport, it doesn’t matter how much CO2 is sucked out of the sky or extracted from the chimney of a factory or power plant, it will be stranded.