Britain's green credibility gap

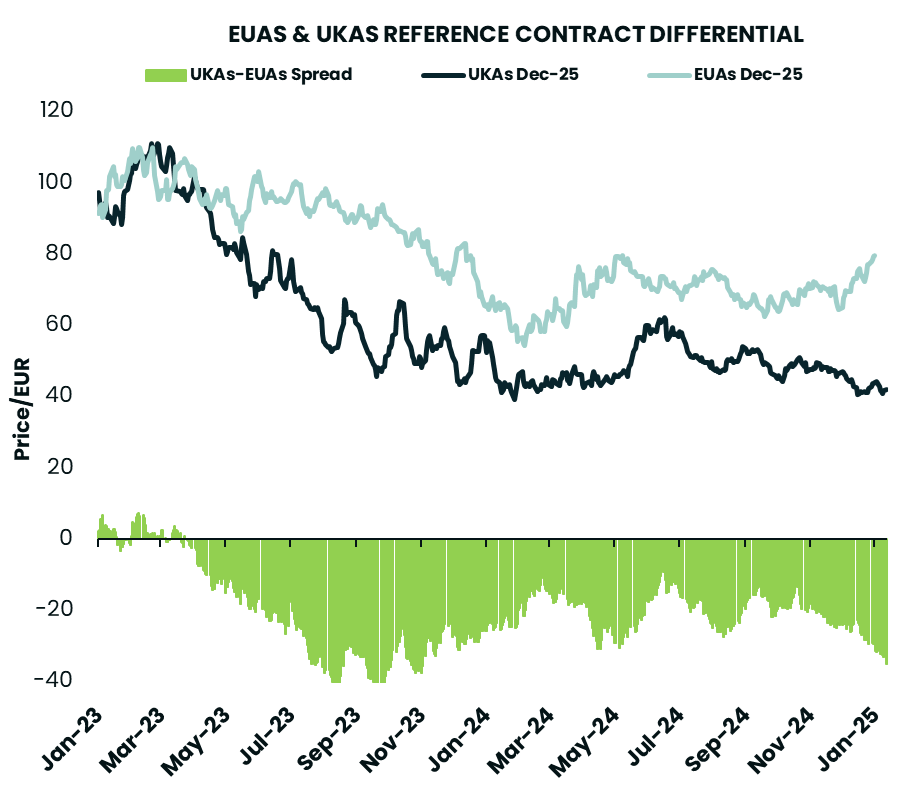

UK carbon price slumps to record low, 50% below the EU

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! 🏭

If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access. By subscribing you’ll join more than 4,000 people who already read Carbon Risk. Check out what other subscribers are saying.

You can also follow on LinkedIn and Bluesky. The Carbon Risk referral program means you get rewarded for sharing the articles. Once you’ve read this article be sure to check out the table of contents [Start here].

Thanks for reading Carbon Risk and sharing my work! 🔥

Estimated reading time ~ 8 mins

The UK carbon price fell to a record low of £31.54 (€37.35) this week. Even more importantly, the UKA discount versus the EUA price has once again ballooned to around 50%. The last time the spread was this stretched was back in September 2023 when then Conservative Prime Minister Sunak canned, or at least pushed back on, many of the governments net zero targets.

Labour’s landslide victory in the 4th July general election promised so much, but has up until now, failed to deliver. For any Carbon Risk readers not familiar with the tragic comedy of errors that is UK politics I’d urge you to check out

. Suffice to say that the last six months or so could perhaps best be characterised (putting it kindly) as ‘muddling through’.Uppermost in the minds of market participants in the UK carbon market was that the country would be electing a party supportive of ambitious climate policies, and one keen to establish much closer links with the European Union; the relationship between the two having been severely damaged by the divorce that was Brexit.

In theory a party more focused on climate policy would move quicker to reform it’s carbon market, bringing it into line with ambitious 2030 and 2050 climate targets. In theory a party keen on building bridges with the EU would rapidly seek to establish a link between the UK and EU ETS, piggybacking on the EU’s climate credibility.

Unfortunately, none of those things have happened. Instead, there’s been more muddling through. While EUAs have jumped by 10% since July to over €80 per tonne in early 2025, the UKA price has slumped by one-third to below €40 per tonne, opening up a chasm between the two markets.