Aluminium's climate paradox

Aluminium is often referred to as “congealed electricity”

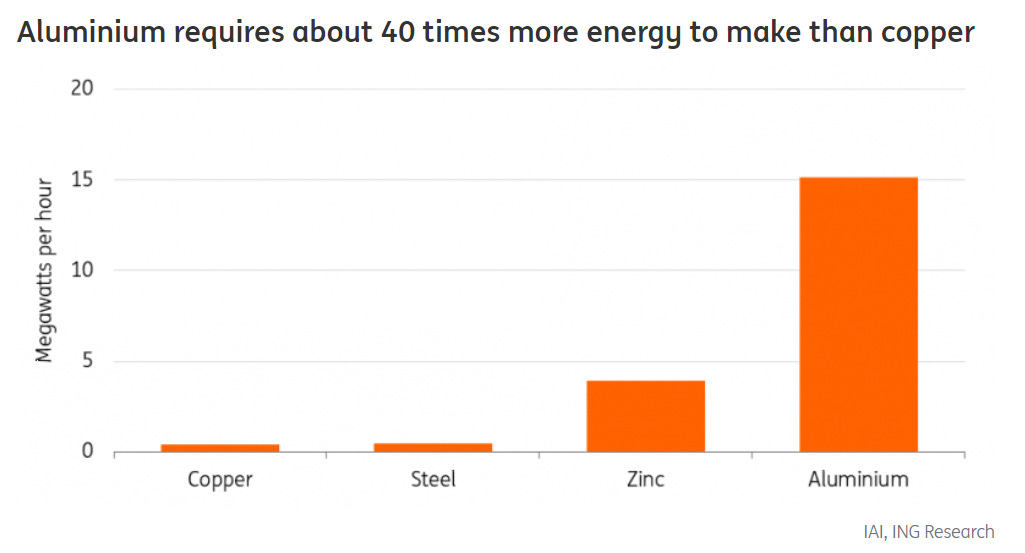

One of the most notorious power hungry industries, it takes about 15 MWh of electricity to produce one tonne of aluminium. That’s more than three times as much energy as zinc and about 40 times more than copper or steel.

Producing aluminium is also highly carbon intensive. On average, mining and processing results in around 15 tonnes of CO2e emitted per tonne of aluminium produced. Overall, aluminium production emits some 1.1 billion tonnes of CO2 per year, accounting for around 2.5% of global emissions.

In addition to the huge power demands, the industry’s reliance on electricity generated using thermal coal underpins why it is so emissions intensive. Aluminium smelters consumed 880 thousand GWh in 2021, according to estimates by International Aluminium. Almost 55% of this electricity was generated via thermal coal (primarily in China), hydropower accounted for 30% (Europe and North America), with 10% coming from natural gas (Middle East), and the remaining 5% split between nuclear and other renewables.

Power source used by primary aluminium smelters, 2021

7-8")

“Miracle metal” must do better

Aluminium production is highly carbon intensive, yet without aluminium decarbonisation cannot take place. To see why, consider it’s attributes. Aluminium is lightweight but strong, good conductivity, resistance to corrosion, elasticity and easily recyclable. Aluminium has more than one nickname, and if the metal had feelings it would probably prefer it’s other name - the “miracle metal”.

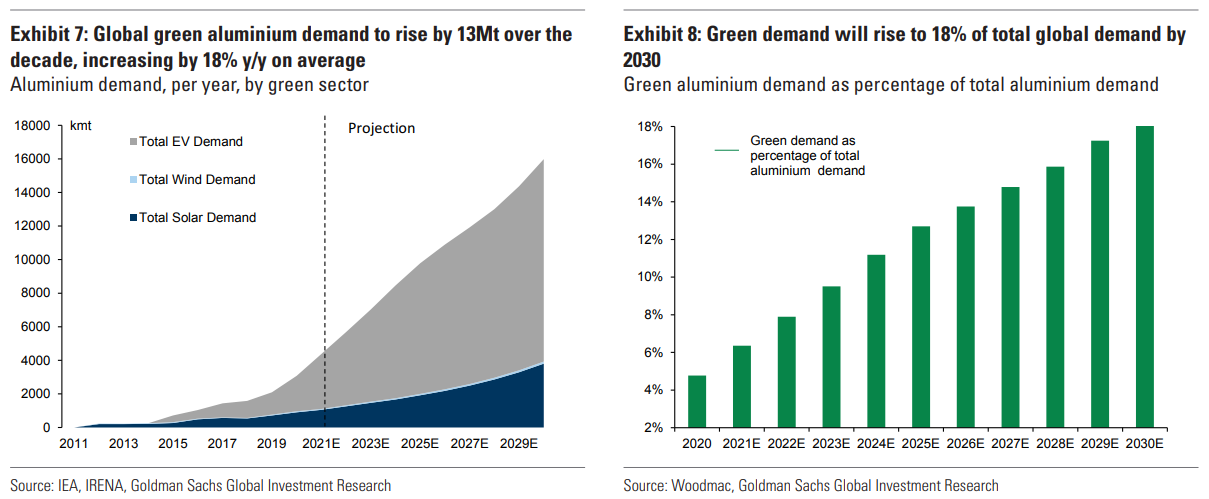

Global demand for the metal could grow 50% to 108 million tonnes by 2050, according to recent projections by CRU. Growth in demand will be supported by population growth and industrialisation, but also due to its vital role in enabling the energy transition: it is used to lightweight electric vehicles, vital in solar power generation, green buildings and electricity cabling. However, the highest growth in terms of absolute demand is expected to come from the shift in the transportation sector to EVs.

Despite its good side, the “miracle metal” cannot escape its own carbon footprint being scrutinised by automobile manufacturers, governments and investors (see 'Green' lithium).

There is increasing pressure from manufacturers with action-oriented climate targets to procure low carbon aluminium, also commonly known as “green aluminium”. Low carbon aluminium is defined as emitting 4 tonnes of CO2 or less, one-quarter of the global average carbon emissions from aluminium production.

Automobile companies, particularly European manufacturers are at the forefront of this trend. For example, Porsche recently announced a deal to supply with Norwegian aluminium and renewable energy company, Norsk Hydro to supply it with low carbon aluminium. In 2022, rival German car company, Mercedes also announced a similar deal with Norsk Hydro. Meanwhile, BMW's North American factories will receive aluminium sourced from Rio Tinto's hydro-powered aluminium operations in Canada.1

All of these deals help to drastically cut the embodied emissions in their vehicles. For example, the aluminium used in Porsche’s Taycan electric sports car, which already consists of about 30% aluminium by weight, will soon be produced using 60% less emissions than the European average. Global demand for low carbon aluminium is projected to increase from 23 million tonnes in 2021 to 62 million tonnes by 2030, according to McKinsey. Demand to reduce emissions even further is growing, especially from the luxury automotive and energy generation sectors.

Drought could scupper further declines in emission intensity

Global production of low carbon aluminium is expected to grow from 44 Million tonnes in 2021 to 71 million tonnes in 2030, according to McKinsey. However, future growth in low carbon aluminium supply is primarily dependent upon the availability of hydropower, the economic sustainability of which is brought into question by one of the main threats posed by global warming - prolonged high temperatures and persistent drought.

Global supplies of low carbon aluminium dipped in 2022 as drought in southern China forced Yunnan province authorities to order aluminium smelters to lower production in order to help balance the power system; first by 10% in September last year, then by 20%, and most recently by 40% as the drought worsened. Smelters had been lured to Yunnan due to the availability of cheap hydro power - around 80% of Yunnan’s electricity comes from hydropower. By 2022, smelters accounted for an estimated 30% of electricity consumption across the province.2

China is the dominant global supplier of aluminium, accounting for over 55% of production, while Yunnan province accounts for 12% of the country’s capacity. What happens in Yunnan matters, especially in a world where demand for low carbon aluminium is high and set to grow. Although China has ambitious plans to expand its renewable energy generation, the interconnectedness of its aluminium and hydropower generation sectors, and the increased frequency with which drought affects Yunnan, suggests that China may struggle to reduce the emissions intensity of its aluminium. That may leave it lying uncompetitive relative to other, lower carbon suppliers of aluminium.

Meanwhile in Europe, hydropower generates around 650 TWh of electricity per year, of which some 15% of this is consumed by the continents aluminium smelters, many of which are located in Norway - the largest supplier of aluminium to the EU in 2022. Norway didn’t escape the drought that afflicted much of central Europe last year. Low reservoir levels cut hydropower generation to it’s lowest level in 20 years (see The forgotten giant of clean energy: Why carbon market investors need to keep an eye on Europe's drought).

Europe also relies on imports from Russia, Turkey, Mozambique and South Africa. The aluminium produced from these four countries are all near the European average emissions intensity and considered low carbon aluminium due to their use of hydropower generation.

Key suppliers of aluminium to the EU and their emission intensity

Lingering impact of sky-high European power prices

It’s worth remembering that the sky high power prices seen during 2002, and particularly during the height of summer were partly due to the severe drought in Europe and the adverse impact it had on hydropower and nuclear power output.

Western European aluminium output fell 12.5% between 2021 and 2022 as record power prices forced operators of aluminium smelters to cut production or mothball their plants. Aluminium output in December dropped to 2.73 million tonnes (on an annualised basis), down by 540 thousand tonnes on December 2021 (down 16.5%), and the lowest production rate this century (see Power down: Why the outlook for European electricity consumption will be crucial in determining carbon prices in 2023).

The impact of those record power prices looks set to linger.

Aluminium Dunkerque Industries France, Europe’s largest aluminium smelter is perhaps the sole plant expected to restart curtailed capacity (60 thousand tonnes per year) by the end of May, following intervention from the French government.

The challenge facing smelter operators is that although power prices have come down, they are still high by historical standards, and even if they bring back production (a long and costly process), there are no guarantees that there will be sufficient demand for them to profitably sell into. And even if they manage to restart production they face the risk of a rebound in power prices, especially if there is another drought this summer. Norsk Hydro warned that a further 600 thousand tonnes of European aluminium smelting capacity could be at risk if prices were to spike again.

The outlook is grim for those smelters that are not on a long-term power contract set at pre-energy crisis levels, that are not protected by government subsidies or have access to their own renewable energy supplies. However, if Europe doesn't have the basic industries in place, they stand no chance of building the industries of tomorrow, and especially those industries required to enable the energy transition. In response to concerns that Germany would lose access to these vital building blocks, the German government recently announced that it would provide billions of euros in state support to guarantee lower energy prices for energy intensive companies through to 2030.3

Aluminium is a climate paradox.

Highly carbon intensive due to the prevalent use of coal, aluminium is essential to decarbonisation - especially the growth in EV’s and solar generation.

Yet, reducing aluminium’s emissions requires an increased reliance on hydropower, but this means being increasingly exposed to the drought conditions that have become more intense under a warmer climate.

Meanwhile, persistent drought has led to dramatic power price spikes in Europe and elsewhere as low water levels led to weak hydropower generation and limited nuclear output.

High power prices threaten the financial sustainability of the remaining aluminium smelters. For those that remain, a switch to thermal coal generation supported by state subsidies may be the only way to survive.

More than a climate paradox, aluminium is stuck in a vicious circle.

https://www.reuters.com/business/autos-transportation/norsk-hydro-supply-porsche-with-low-carbon-aluminium-2023-04-26/#:~:text=OSLO%2C%20April%2026%20(Reuters),the%20companies%20said%20on%20Wednesday

https://www.reuters.com/markets/commodities/rio-tinto-enters-agreement-with-bmw-provide-hydro-produced-aluminum-2023-02-21/

https://www.hydroreview.com/environmental/drought-hits-hydropower-supplies-for-chinese-aluminum-smelting-hub/

https://www.cleanenergywire.org/news/german-economy-minister-wants-lower-industry-electricity-costs-billions-subsidies