The trend is your friend in California but could there be a sting in its tail?

California is not cutting greenhouse gas emissions fast enough to meet its self-imposed 2030 target.

In particular, the state faces the trilemma of balancing expanding intermittent renewable energy generation, ensuring adequate energy supplies, and the risk of blackouts as its fragile power grid is buffeted by natural disasters.

As long as this bottleneck remains, the trend for CCA prices is likely to be up…

…But, as regular subscribers of Carbon Risk will know, the price of carbon emission allowances is a not simply a function of abatement costs, the available supply and demand of allowances matter, a lot. The second part in this series of articles focuses on the potential risk looming on the horizon for the Californian carbon market and will be published later this week. To read it, you will need to upgrade to being a paid subscriber.

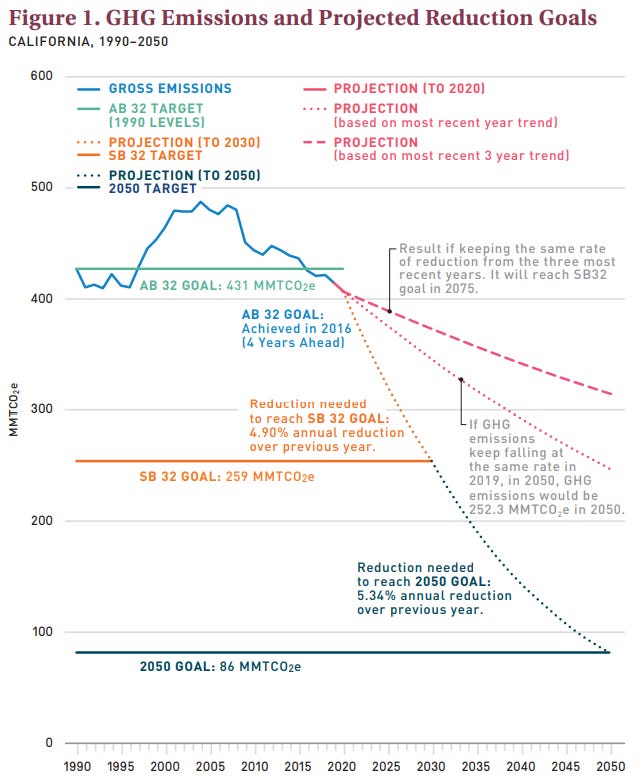

The 2021 California Green Innovation Index, published by the non-profit group Next 10 and prepared by Beacon Economics, reveals that California cut its greenhouse gas emissions by only 1.3 % per year between 2017 and 2019, far below what is needed to meet the states 2030 greenhouse gas emission reduction goals, known as SB 32.

At the state’s current rate of progress, California won’t hit that target until 2063! In order to meet the 2030 goal, the state would need to more than double the annual rate of emission reductions to 4.3%.

What is SB 32?

SB 32, known as the California Global Warming Solutions Act of 2016, requires the California State Air Resources Board (CARB) to ensure the state’s greenhouse gas (GHG) emissions are reduced to 40% below the 1990 levels (259 MMT CO2e) by 2030.

SB 32 follows on from AB 32, signed in 2006. AB 32 required California to reduce its GHG emissions to 1990 levels (431 MMT CO2e) by 2020. The state reached that goal by 2016.

California has a longer term goal of cutting emissions to 86 MMT CO2e by 2050, 80% below 1990 levels.

Around 45% of the states cap-and-trade direct allocation to regulated entities covers utilities - power generation and distribution. As such the roll out of renewable energy generation is one of the most important trends to watch if emission targets are to be met. At present, the pace of renewable adoption shows California is lagging behind where it needs to be if 2030 targets are to be met.

California’s total power mix (in-state generation plus imports) from renewable sources rose by 1.4% to 33.1% in 2020, barely meeting the interim renewable energy generation goal of 33%. Indeed, it only met this due largely to the retirement of older, less efficient fossil fuel generation, as opposed to the addition of new renewable generation. However, to meet the 2030 goal of 60%, California’s share of electricity generation from renewables would need to increase by around 2.5% each year through to 2030.

California faces the same challenge that Europe has in its drive to meet ambitious climate targets, namely the intermittent limitations of renewables and the need to simultaneously ensure sufficient power supplies at all times. As in Europe, the quickest way for California to ensure supplies when there is insufficient wind and sun is to fire up gas fired power generators. Furthermore, California also faces the threat of natural disasters - drought, and wildfires - that threaten renewable generation and the resiliency of the grid. A much more acute challenge that that faced over in Europe.

The present day limitations of renewable energy generation in California (i.e. the need to burn natural gas to balance solar, wind and hydro) runs counter to the state’s emission reductions target. Last year natural gas accounted for nearly half of California’s in-state electricity generation as new gas fired power generation came onstream.

Another important sector to keep an eye on is transportation. Emissions from the transportation sector fell sharply in 2020 due to covid-19 related lockdowns (down 15% across the USA as a whole, according to the EIA), however national level data also suggests 2021 transport emissions may be already higher than 2020. Although the share of state emissions from transportation is around 41%, the manufacture of transport fuels (e.g. by refineries) accounts for 18% of direct allocation allowances under California’s ETS.

It’s here that paying attention to the role of direct regulation in cutting emissions will be important in gauging the impact on carbon market fundamentals. In particular, the Low Carbon Fuel Standard (LCFS) is a key part of a comprehensive set of programs designed to cut emissions and other smog-forming and toxic air pollutants in California. The LCFS is designed to decrease the carbon intensity of California's transportation fuel pool and provide an increasing range of low-carbon and renewable alternatives, which reduce petroleum dependency and also achieve air quality benefits.

Meanwhile, new targets and commitments announced in 2020 by both the state and federal government should help further the adoption of clean vehicles in California. For example, in August 2021, President Biden announced a goal that 50% of new vehicle sales should be zero-emission vehicles (ZEVs) by 2030. The state can anticipate emissions reductions from the heavy-duty sector thanks to the Clean Trucks Rule (July 2020) and a state budget investment of $1.4 billion in zero emission vehicles (ZEVs), which includes funding for ZEV heavy-duty trucks.

In the first phase of CARB’s plans (ending in 2020), California’s ETS accounted from some 15% of all emission reductions achieved by the state - although estimates differ markedly, and tend to suggest carbon prices had even less impact on abatement. The low hanging carbon reduction fruit achieved came from utilities that cut their use of imported power from out of state coal plants.

However, for California to meet its 2030 target, and 2050 thereafter the carbon market will have to do much more of the heavy lifting. Indeed, in their most recent scoping plan for 2030, CARB outline that they expect the carbon market to be responsible for almost half (47%) of the cumulative emission reductions required, some 3 times the impact so far.

On the face of it that is a powerful tailwind for carbon prices in the Golden state. Part 2 in this series of articles focuses on the potential risk looming on the horizon and will be available for paid subscribers to read later this week.