Stranded asset, or last mover advantage?

“Stranded assets” are those left unexploited or experience a decline in value due to changing in market conditions and regulations adopted to decarbonise the economy.

The energy supply and generation business is particularly familiar with the concept of stranded assets. The total embedded emissions of known fossil fuel reserves is estimated to be around 3,700 Gt CO2, according to Carbon Tracker. If all reserves were produced this would lead to global temperatures rising in excess of 3°C. To limit warming to 1.5°C, 90% of fossil fuel reserves must remain in the ground, thus becoming a “stranded asset”.

Stranding is a function of changed consumption and expectations influenced by changes in policy, pricing, technology and behaviour. One or a combination of these factors could make it relatively more expensive to produce and consume than the alternatives, e.g. via carbon pricing and taxes, regulation, etc. These factors could make it uneconomical to invest in increasing supply, or face adverse reputational effects if they do. The technologies available to asset owners influence the timing of investment decisions, e.g. infrastructure investment involves long lead times, long lifetimes, and new technology especially, involves uncertain payoffs.

And finally, the behaviour of asset owners cannot be considered in isolation, since their behaviour operates in an environment where the incentives are not always clear and consistent, e.g. while publicly traded companies are subject to the criticism of their shareholders, state run companies may also have to consider the impact of their actions on employment and social stability.

However, as the the energy crisis of 2022 demonstrates, it’s not as easy as simply leaving fossil fuels in the ground and letting the energy transition take care of itself. Timing the inflexion point between traditional energy sources (natural gas, coal and to a lesser extent oil) and renewables, allied with deciding the role of nuclear is fraught with difficult political, economic and technological decisions.

In the rush forward, governments underestimated the risks to their own energy security. That decision gave rise to renewed geopolitical risks and concerns that people - not only those living in poor developing countries - would have the energy and food to survive.

Steel faces its own stranding risks

It’s not only fossil fuels that face the risk of becoming stranded assets in a carbon constrained future. The steel industry, responsible for 7-9% of all direct emissions from fossil fuels is another.

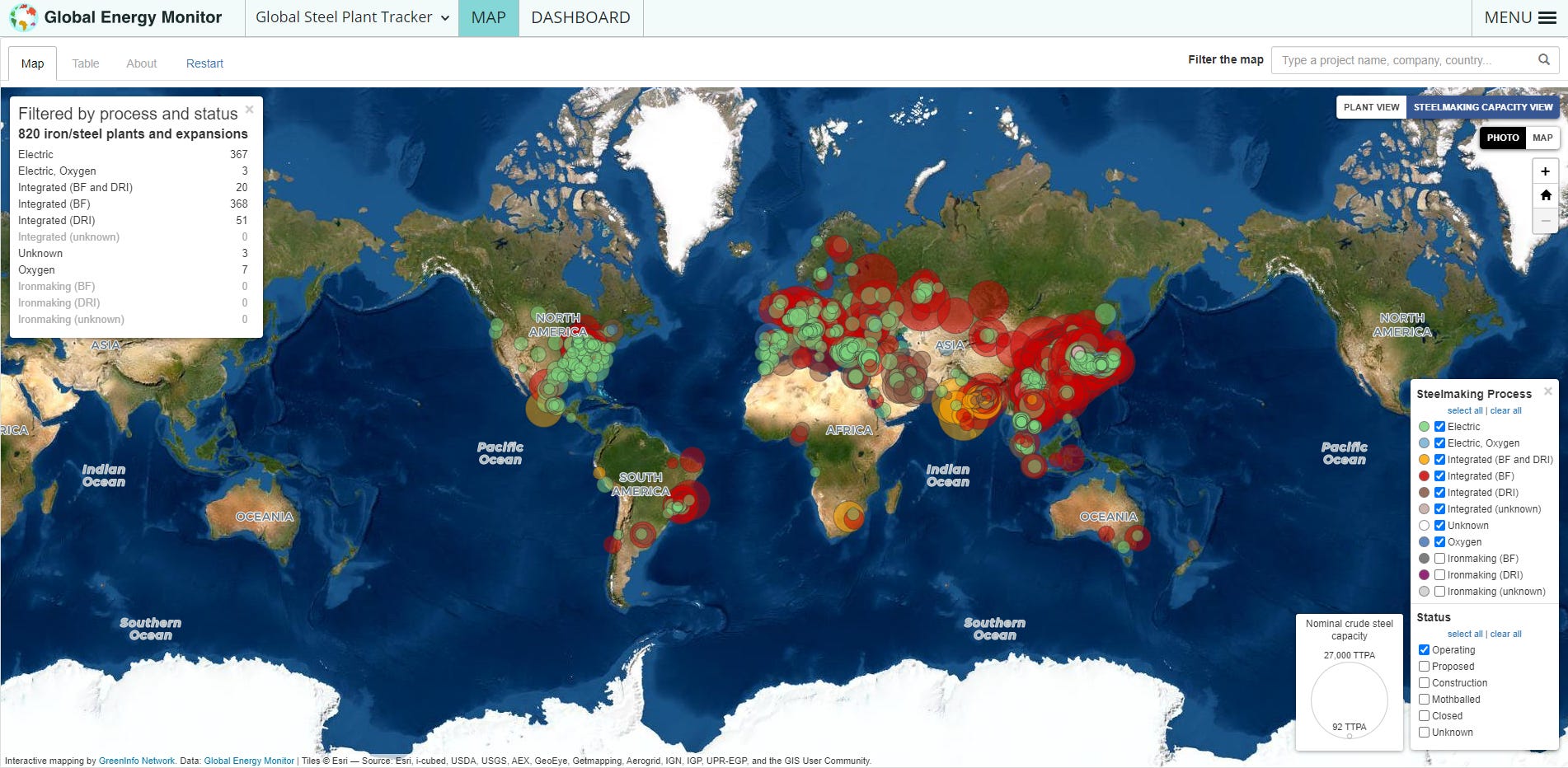

According to the Global Steel Plant Tracker (GSPT), approximately 69% of known global crude steel capacity currently uses the basic oxygen furnace (BF) route, 31% uses electric arc furnace (EAF) steelmaking, and less than 1% uses open hearth furnace (OHF) steelmaking.

In 2019 the global steel industry emitted over 3.6 Gt CO2 emissions, including 2.6 Gt of direct CO2 emissions per year and nearly 1.1 Gt of indirect CO2 emissions from the power sector and combustion of steel off-gases. Approximately 86% of these emissions came from BF steel production, despite accounting for around two-thirds of production, while 14% came from EAF steel production.

Producing one tonne of steel via BF emits around 2.2 tonnes of CO2 and requires roughly 20.8 GJ of energy, assuming global average electricity carbon intensity. In comparison, scrap-based EAF production results in approximately 0.3 tonnes of CO2 per tonne of crude steel (not including embodied emissions), and requires 9.0 GJ of energy. Hydrogen, natural gas and coal can also be used in EAF, but this increases average emissions to around 0.7, 1.4 and 1.8 tonnes of CO2 respectively.

Crude steel manufacturing capacity is largely concentrated in Asia, with China accounting for 49% (1083 Mt) of operating steelmaking capacity. However, when considering only BF steelmaking, China accounts for 60% (804 Mt) of global operating capacity.

Map 1: Global steelmaking capacity by type - operating

Fold, check or raise?

There is no single silver bullet to decarbonise steel production, not yet at least. That means the decision to invest in new technology, or stick with what they already have is far from an easy one. Options include shifting completely to electrification and increased use of recycled steel (via an EAF), or progressing to more technologically advanced solutions such as direct reduction with hydrogen and smelting in the EAF, alkaline iron electrolysis, the HIsarna smelting reduction process, or CO2 capture and utilisation of waste gases from integrated blast furnaces.

By 2030, 1090 Mt of existing coal-based blast furnaces (77% of the BF fleet in the GSPT) will reach the end of their working life and the start of their next reinvestment cycle. The average investment cycle for BF under typical operation and maintenance is approximately 15-20 years. China alone accounts for 730 Mt of this BF capacity requiring reinvestment.

Over the next decade, steel plant owners will need to decide whether to refurbish their BFs (which involves relining the furnace), or shut them down. The cost to refurbish a typical BF is around one-third to one-half of a new blast furnace and results in substantial revenue loss during refurbishment. Overall, the cost of a BF refurb including lost earnings is estimated to be around $1.3 billion and last three months. However, the reinvestment cycle for blast furnaces typically decreases with each subsequent relining, and so this isn’t something operators can do more than a couple of times, at least not economically.

As the end of a BF’s lifecycle approaches, plant owners face a quandary. Do they close the facility, refurbish it to extend it’s life, or invest in new low-emission steel making technology.

Global steel sector likely to miss net-zero target

The share of EAF steelmaking capacity needs to reach 37% by 2030 and 53% by 2050 in order to meet the IEA’s Net-zero by 2050 scenario. This compares with the current mix of operating steelmaking capacity which uses 69% BF and 31% EAF. Taking account of the projected 12% increase in demand for steel by 2050, an additional 576 Mt of EAF capacity needs to be added, while 419 Mt of BF capacity needs to be cancelled or retired.

However, of the 600 Mt + steelmaking capacity under development, 67% of the known steelmaking processes uses high carbon BF technology, and only 33% uses low carbon EAF steelmaking. However, of those steel projects under construction with known processes the BF share jumps to 72%, while only 28% is EAF. If the global steel sector is serious about decarbonising, they are not showing it in their investment intentions.

China and India account for over two-thirds of new steel plants proposed and under construction. Despite both countries committing to Net-zero by 2060 and 2070 respectively, 80% of new BF capacity is expected to be built in China and India.

Map 2: Global steelmaking capacity by type - proposed and under construction

Stranded asset, or last mover advantage?

GSPT estimates that around 132 Mt of existing BF capacity is at risk of being stranded by 2030, rising to 514 Mt by 2050. The capital cost at risk of being stranded is in the region of $500-$770 billion, with much of this hit being taken by China and India.

Despite the risk of stranded assets, both China and India have an incentive to continue to use BF technology for as long as possible. Both countries have significant thermal and coking coal reserves, to power and supply feedstock to their steel plants. That gives them an economic advantage compared with other major producers who may need to import supplies from elsewhere in the world. They both have vast domestic markets that are likely to see further strong demand growth for steel.

The steel manufacturing sector also supports hundreds of thousands of jobs across China and India. As in other parts of the world, steel manufacturing often dominates employments for whole regions meaning that plant closures can have adverse social and political consequences. BF plants typically employ far more people than EAF steel plants. Switching to lower carbon steel manufacturing would inevitably result in job losses. State owned and managed steel plants also tilts the incentives to prolong the life of BFs even longer.

The final and most important factor in pushing China, India and other countries with substantial BF capacity is “last mover advantage”.

Last mover advantage in this example means that steel manufacturers decide to wait as long as possible before choosing a low carbon steel technology. As I mentioned earlier, BF steel plants can retrofit their plants a number of times before having to make a final decision on their future investment.

While other countries may go straight to EAF, those who wait can benefit from the experience of those that went before them, avoiding their mistakes. When it comes to infrastructure that lasts twenty or more years it’s important not to jump at the only technology available.

I’ve written previously about Wright’s Law (see The long term price of emission). Predating Moore’s Law by almost thirty years, it forecasts cost as a function of the number of units produced. Essentially, learning by doing results in cost efficiencies and improvements.

The EU and other regions forced to move quickly to decarbonise their steel sector are unlikely to benefit from this process. Each firm has to pursue their own strategy simultaneously, under high pressure to meet targets, but what this means is that they cannot benefit from the experience of others in the process.

For China and India, rather than left holding stranded assets, may actually hold a crucial last mover advantage. They can continue to produce low cost steel in the meantime but will then switch to low carbon steel when the opportunity is right and the optimal technological solution becomes clearer.

Steel is a significant emitter of carbon dioxide, but it is also a crucial ingredient in the infrastructure the world needs to decarbonise. Each new MW of solar power requires 35-45 tonnes of steel, and 120-180 tonnes for each MW of wind power. The decision to wait could give China and India a crucial increase in market share as demand for steel continues to grows.