The convergence trade

What's behind the collapse in the UKA-EUA carbon market spread?

The UKA-EUA carbon market spread has dwindled from €32.80 per tonne (~42%) in early September to less than €2 per tonne by late November.

Two factors have contributed to the narrowing in the spread: political uncertainty over the UK governments commitment to its 2050 net zero goal, and an increase in UKAs available to meet hedging demand from UK power generators.

Why is this important? Well, many carbon market investors are likely to be exposed to the UK market. For example, the KraneShares Global Carbon Allowance ETF (KRBN) has approximately 5% exposure to the UK carbon market. Meanwhile, around one-quarter of AUM in the Ninepoint Carbon Credit ETF (CBON) are allocated to the UK.

The UK had been one of the standout performers among compliance carbon markets. In the twelve months to mid-August this year, UK carbon prices more than doubled, compared with an 80% increase for the EU carbon market.

Let’s start off with the political uncertainty. A little under halfway through the Liz Truss Premiership (20 days to be precise), the UK government announced that it would commission an independent review of the country’s 2050 net zero delivery goals.

Justifying the decision, the government cited how “the Russian invasion of Ukraine and other global factors have fundamentally changed the economic landscape in the UK, placing huge pressure on households and business through high energy prices.” The overarching aim of the review was to ensure that the governments net zero approach is “pro-business and pro-growth”.

The first stage of the three-month review - a public consultation - closed on 27th October. The review, including a set of recommendations, is expected to be published by the end of the year.

Although politicians have not mentioned the UK ETS, it is no secret that the UK’s largest carbon emitters have been paying significantly more than their competitors in the EU. Since the UK ETS launched in mid-May 2021 UK obligated emitters have been paying approximately 13% more than EU firms, although as I noted above that has narrowed significantly in the past couple months.

Remember, the UK also has an additional domestic top-up carbon tax levied on power generators. This is on top of the UK ETS carbon price. The Carbon Price Support as its known was introduced in 2013 at £16 per tonne, and although it was set to rise to £30 by 2020, the government decided in 2018 to cap it at £18.08 per tonne (~€21 per tonne), from where it has remained unchanged ever since (see Why carbon investors need to pay attention to the UK carbon market).

Up until the summer there was a high degree of confidence in the UK governments commitment to a strong carbon price. Recall, that the governments response to the recent UK ETS consultation indicated that they “intend to legislate to align the cap to a net zero trajectory in 2024.” To do so, many were expecting a large one-off downward adjustment in the emissions cap to take place in 2024 (see The UK carbon market continues to dodge political headwinds...but for how long?).

However, the UK carbon market is currently in a state of political uncertainty. In addition to doubts about the one-off adjustment, the government has still not specified how the emission cap will decline during the period 2024–30. The government perhaps fearful that if they proceed with the original plan then UK carbon prices would rise sharply. That’s potentially problematic for businesses should they still be buffeted by high energy prices next winter and the one after that.

The second factor contributing to the narrowing in the spread is the increase in availability of UKAs for hedging demand from the UK power sector. In the interim period between the UK leaving the EU and the launch of the UK ETS, UK utilities had to use EUAs to hedge their power generation carbon liabilities. It was far from perfect as a hedge, but the only one that was available at the time.

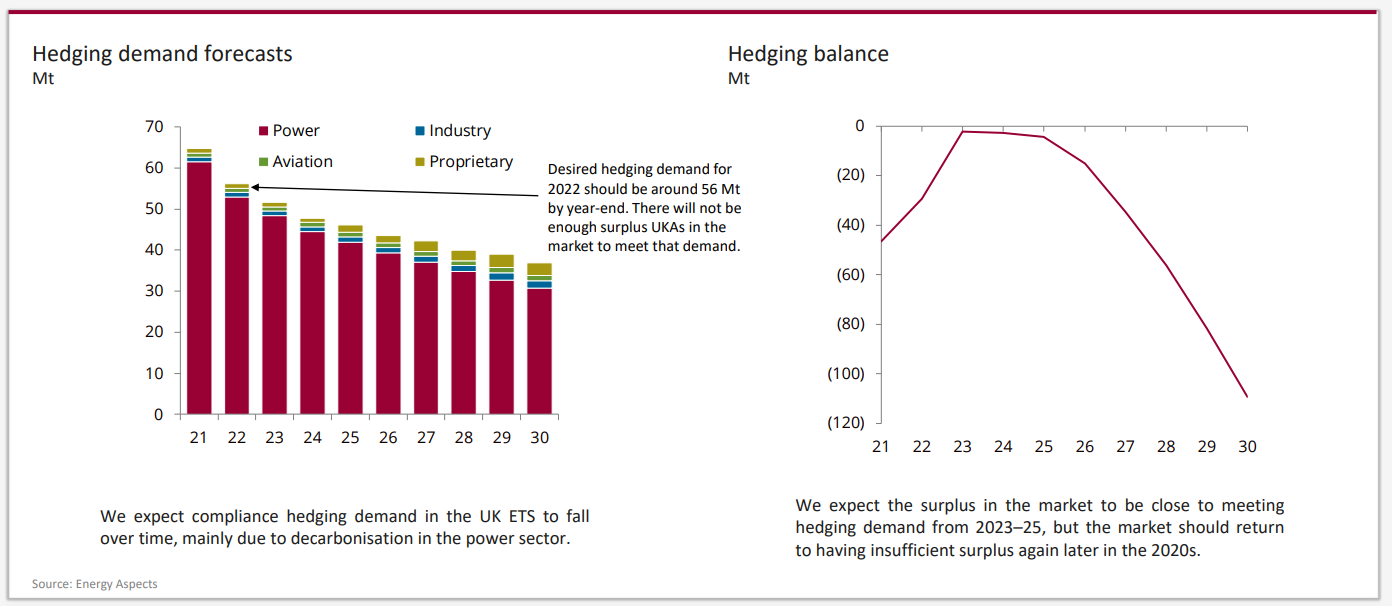

Now though, after a number of fortnightly auctions have taken place, the number of UKAs available in the market has increased, making it easier for UK utilities to hedge their requirements, in turn easing the pressure on the UKA-EUA spread. There should be sufficient UKAs in the market to meet hedging demand over the next couple of years, according to Energy Aspects.

Even though hedging demand is likely to fall as the UK power sector decarbonises, the prospect of a one-off downward adjustment in the emissions cap in 2024, coupled with annual declines thereafter is expected to mean UKAs available for hedging are insufficient to meet demand. This might mean that the UKA-EUA spread balloons out again during the second half of this decade.

However, that all depends on whether the UK government determines that it’s Net Zero Strategy - including the UK ETS - is consistent with being “pro-business and pro-growth”.

In Commitment issues I argue that once governments lose trust in one arena of policy they can quickly lose it in another. The UK’s massive fiscal splurge, made worse by the circumvention of the Treasury’s commitment device - The Office of Budget Responsibility (OBR) - undermined trust in the UK’s fiscal responsibility. The episode resulted in a sell-off in government bonds and a sharp rise in yields, increasing the interest rate by which the UK government and much of the rest of the economy could borrow at.

In that piece I concluded that once the market senses commitment issues extend to climate policy too then the cost of meeting targets will get even more expensive, and the chances of hitting them less likely. Key to that is a strong carbon price. As the UKA-EUA spread continues to narrow, the UK government may find that the costs to commitment issues extends far wider than just higher interest rates.