Picking the ‘low hanging fruit’: Technology key to North Sea methane abatement

Welcome to Carbon Risk — helping investors navigate 'The Currency of Decarbonisation'! If you haven’t already subscribed please click on the link below, or try a 7-day free trial giving you full access.

By subscribing you’ll join more than 3,000 people who already read Carbon Risk. You can also follow my posts on LinkedIn and benefit from my referral program. Thanks for reading!

Estimated reading time ~ 11 mins

A wealth of new technology and analytics tools are helping the industry slash methane emissions - and removing any excuses around inaction.

UKCS upstream methane intensity - the percentage of methane emitted per unit of oil or gas produced - has declined by about 40% since 2018

Overall UKCS methane emissions are likely to be an underestimate, as conventional forms of measurement face limitations

Remote monitoring technology – satellites in particular – coupled with advanced analytics are supporting more accurate and timely measurement

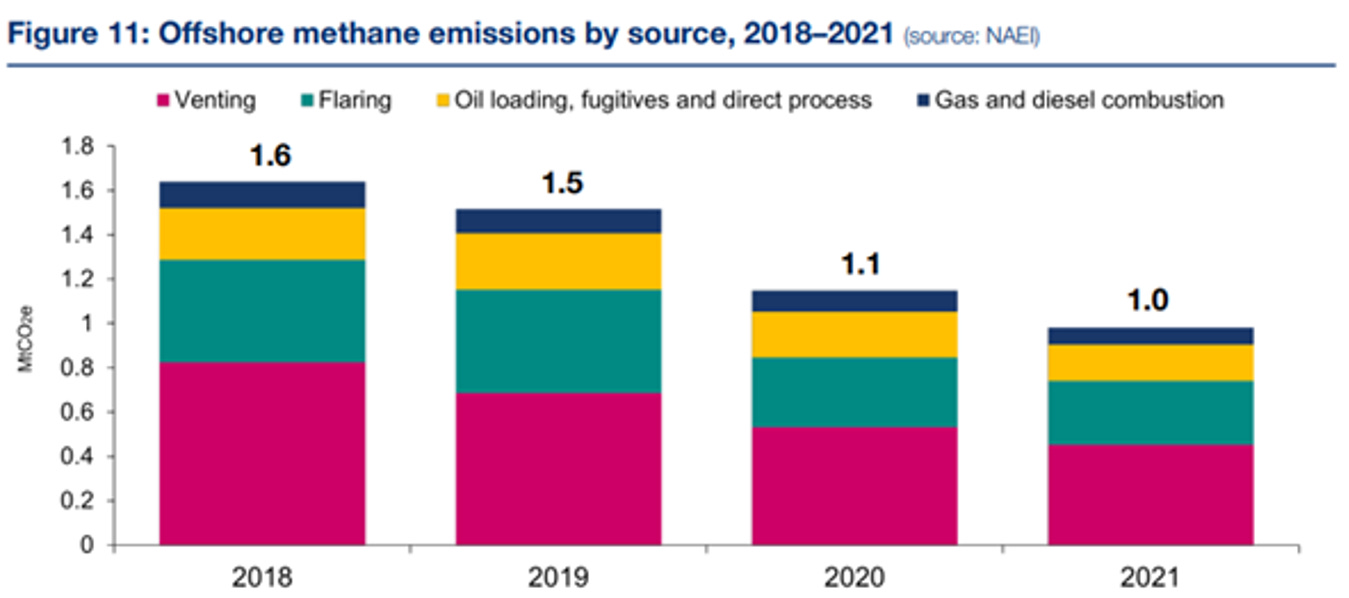

The UK offshore oil and gas industry has made significant progress in cutting its methane emissions. Since 2018 methane emissions have declined by 40% to 0.98 million tonnes of CO2 equivalent in 2021, according to data from the National Atmospheric Emissions Inventory (NAEI).

A decline in gas production, maintenance activity, and improvements in the efficiency of equipment and leakage detection systems have all contributed to declining methane emissions, according to a recent report from the North Sea Transition Authority (NSTA). Yet provisional estimates for 2022 based on Environmental Emissions and Monitoring System (EEMS) data, indicates that the decline may be starting to plateau, with emissions only dropping by 1%.

Nevertheless, research published by academics from Colorado State and Princeton Universities suggests that the NAEI’s methane emission estimates are significantly underestimated. The study covered oil and gas extraction, transport by pipeline, and activity at onshore terminals and so covers a broader scope of activities than illustrated in the chart above.

The researchers posit that since the NAEI’s ‘bottom-up’ approach only accounts for emissions from “processes and activities designated as emission sources and for which emission factors exist,” it cannot account for every source of methane. While 2019 NAEI data gives an overall methane intensity estimate of 0.14%, the study which is based on a ‘top-down’ approach to measurement suggests that this should be 0.72%.

What gets measured

Access to frequent and consistently measured emissions data is vital if UKCS operators are to continue to cut methane emissions from their upstream facilities. The NSTA is working with the Offshore Petroleum Regulator for Environment and Decommissioning (OPRED) to help industry increase the accuracy of these measurements.

One of the most important actions is increasing the number of flare and vents that have meters installed. Most flares have these equipped, though historically vents do not. However, the latter represent a far smaller proportion of emissions and priority has tended to be placed on larger sources.

The UK is unlikely to be alone in underestimating methane emissions from the oil and gas industry. In 2022 the International Energy Agency (IEA) published a report showing that national inventories underestimate energy sector methane emissions by 70%. Furthermore, a growing body of research suggests that estimated methane emissions from offshore oil and gas facilities elsewhere in the world may also be skewed to the upside.

The potential for underestimating methane means that care must be taken when comparing different jurisdictions based on official reported data. Very few countries report upstream methane emissions by source. Those that do, such as the UK, Norway and the US typically use different methodologies, source categories and exclusions. This makes direct comparison and quantification difficult - something that will become more important as regulations begin to tighten.

Pressure for change

Up until recently, the only country to penalise methane emissions was Norway. Its government introduced a tax on oil and gas sector methane emissions in 1991. In 2022 the tax was set at an eye watering NOK 766 per tonne CO2e (equivalent to $71).

In August 2022 the US government announced that it would be introducing a methane fee on its oil and gas industry. The charge came into force at the start of 2024 at $900 per tonne of methane ($36 per tonne of CO2e) and is set to rise gradually to $1,500 a tonne ($60 per tonne of CO2e) in 2026.

In late 2023 EU policymakers signed off on the EU Methane Regulation, the bloc’s first legislation specifically targeting methane emissions from the energy sector. In addition to bans on routine venting and flaring, the regulation will impose methane emission intensity limits on imports of fossil fuels into the EU. If imported oil and gas fails to meet a maximum methane intensity threshold the importer will be stung with a financial penalty.

The oil and gas industry are also stepping up their own commitments. At the UN COP28 climate conference in December, 50 major oil and natural gas producers signed an agreement to cut methane intensity to 0.2% by 2030, while also eliminating routine flaring. The 50 signatories include many that are active in the UK North Sea. For example, national oil companies (NOCs) such as CNOOC, and international oil companies (IOCs) including BP, ExxonMobil, and Shell.

The Oil & Gas Decarbonisation Charter (OGDC) as it’s known was the first time that several NOCs have pledged to reduce their operational emissions. Despite this the OGDC was criticised by many NGOs for falling short of the ambition signalled by the same signatories elsewhere. For example, members of the Oil and Gas Climate Initiative (OGCI) have committed to a methane intensity target of “well below” 0.20% by 2025, five years earlier than outlined in the OGDC.

While large single-source emissions may garner headlines, ‘snow-ballers’ such as leaking valves, pneumatic devices, venting from tanks and wellheads and incomplete combustion in generators and flare stacks can also have a significant cumulative impact.

Eyes in the sky

As governments look to tighten methane regulations, the pressure to adopt consistent measurement methodologies is likely to increase, especially where it affects cross-border trade in oil and gas. As such there is an increasing focus on technology – and satellites in particular - to support more accurate and timely measurement of methane emissions.

There are currently three main classes of greenhouse gas (GHG) monitoring satellite. Class 1 is the oldest and provides high–quality data on average GHG concentrations in large geographic regions. For example, the European Space Agency’s TROPOMI satellite. Class 2 satellites are not yet operational but will cover regional–scale emissions. The MethaneSAT project, devised by the Environmental Defense Fund (EDF), is scheduled to launch in the first half of 2024 and will be the first class 2 satellite.

Finally, class 3 satellites focus on point–source emissions, often at the expense of wider coverage. GHGSat, CarbonMapper and PRISMA are examples of satellites designed to provide high-resolution monitoring down to individual industrial facilities.

MethaneSAT aims to monitor at least 80% of global oil and gas production, detecting both concentrated point emissions sources and dispersed emissions. A recent interview by Energy Voice with MethaneSAT’s lead chief scientist revealed that the technology means emissions can be quantified down to an area of just one square kilometre, while picking up sources of methane down to around 500kgs of CH4 per hour. Importantly, the data will be available for online for free, enabling anyone to keep tabs on the industry’s methane emissions.

Technology-based measures are already being put into place to hold oil and gas companies to account for their methane emissions. Shortly after the signing of the OGDC in December, a partnership including the EDF, the UN’s International Methane Emissions Observatory (IMEO), the IEA, Bloomberg Philanthropies, and the non-profit think tank RMI announced that they will use “cutting-edge data” to make methane emissions from oil and gas “visible and quantifiable.”

A key part of this global transparency and accountability initiative will be the MethaneSAT satellite, coupled with data from class 3 satellites that can identify emissions at the facility level.

Methane ‘super-emitters’ - vast plumes of methane releases that exceed 10,000 kg per hour – tend to receive all the media’s attention. Although some may only last a few hours, others may splurge methane for several months. A ‘super-emitter’ can be the result of pipeline or storage tank ruptures, or intentional acts such as direct venting or incomplete combustion.

However, there is a more nefarious type of methane emission event. ‘Snow-ballers’, as they are known, include leaking valves, pneumatic devices, venting from tanks and wellheads, and incomplete combustion in generators and flare stacks. These small-scale operational emissions all add up and can have a huge cumulative impact. It is exactly these types of events that UK oil and gas operators in the North Sea are attempting to identify and abate.

It can be much more difficult to readily identify these emissions remotely. Methane is highly dispersible and so frequency gaps (the time between satellite observations) make it difficult to track down the source. Translating any satellite imaging into facility–level emissions data requires a significant amount of continuous and granular weather and atmospheric measurements at ground level.

Current satellite technology also has trouble detecting methane emitted from offshore operations. Satellites use spectrometers to measure different molecules in the atmosphere but similarities in the absorption profiles of water, methane and other gases make measurements over water, especially in rough seas, particularly difficult. As spectrometer technology develops, the accuracy of satellite methane measurements will improve.

Every methane monitoring solution has its limitations. And so, a combination of approaches is required to provide the most accurate emission estimates, including bottom-up methods (meters, sensors and cameras) and top-down approaches (satellites, drones, etc.).

Harnessing AI

Measurement is one thing, but analysis is quite another. Instead of investing in their own hardware, several analytics companies are using AI to analyse public satellite imagery to extract a trove of precise, actionable, and near-real time information that can be used to inform the oil and gas industry, regulators, and other authorities.

For example, Rystad Energy has developed a field-level, upstream oil and gas methane emissions database that incorporates and combines publicly available methane data, proprietary facility-level estimates, and global satellite data measurements in a consistent manner.

Analysis by the consultancy shows that North America (primarily the United States) and the Middle East (including Iraq and Iran) make up nearly half of global methane emissions from upstream oil and gas activities. Asia (i.e., China and Kazakhstan), Russia and Africa (i.e., Libya, Egypt, and Algeria) make up the vast bulk of the remaining emissions. Europe is by far the smallest contributor to global upstream oil and gas methane emissions.

Yet that doesn’t mean Europe can escape its responsibility. The eyes in the sky will ensure that there is no hiding place.

Kayrros, the digital MRV and environmental intelligence company, harnesses the latest satellite data drawn from the Copernicus network of satellites, coupled with its own proprietary algorithms to deliver near-real time insights on methane emissions. According to data published on its free-to-access Methane Map website, the UK oil and gas industry had an average methane intensity of 0.24 kg per boe in 2022 – some 12 times higher than the Norwegian industry.

In addition to more widespread metering of flares and vents, it’s clear that remote monitoring technology will be crucial if the UK is to narrow the gap with Norway while also meeting its methane emission reduction targets. Many offshore oil and gas operators in the UKCS are already employing remote monitoring technology to monitor methane emissions.

For example, Neptune Energy, operator of the Cygus Platform in the North Sea, has deployed advanced drone technologies to monitor its methane emissions. In 2022 Neptune Energy joined the Aiming for Zero Methane Emissions Initiative, a project developed by the OGCI to cut methane emissions to near zero by 2030.

However, it’s only through broader adoption that measurement accuracy can improve, and actions can be taken to mitigate the emissions. In October 2023, the NSTA and the Net Zero Technology Centre (NZTC) launched a call for emissions measuring and monitoring technologies, giving companies developing these solutions the opportunity to have their product featured in a new roadmap.

Methane abatement by the oil and gas industry is one of the most cost-effective ways to cut greenhouse gas (GHG) emissions. It’s no wonder it’s getting so much attention. For example, the IEA estimates that just over one-third (36%) of the UK’s oil and gas methane emissions could be mitigated at no net cost, based on average 2017–2021 natural gas prices.

Up until recently it has been difficult to identify these opportunities – described by the IEA and others as the ‘low hanging fruit’ in tackling climate change - nor incentivised to fix them. But now, the development of remote methane monitoring, coupled with regulatory and voluntary scrutiny, means that there is no longer any excuse.