France's nuclear winter of discontent

Nuclear generation tends to be uncorrelated with carbon prices. The exception is when high power prices coincide with a period of tight carbon allowance supply.

This August’s surge in European power prices coincided with a sharp increase in EU carbon prices towards €100 per tonne as utilities looked to hedge their power generation, while the supply of allowances via auction was limited.

With renewed concern over the outlook for France’s nuclear generation, tight power supplies could result in a repeat scenario developing as we move into 2023.

Before considering the outlook lets recap why France is in this mess.

In late 2021 France’s state owned energy giant EDF, announced that following a regular ten-year inspection, it’s engineers had uncovered faults at one its nuclear reactors. The discovery prompted EDF to close it and three other similar reactors for unplanned maintenance.

Things were to get much worse in early 2022. EDF announced it had found similar problems at yet another reactor, prompting its closure for repairs, and that it was now extending the maintenance outage period at the earlier four problem reactors.

As a result of its maintenance woes, EDF announced that it was lowering its 2022 nuclear power output forecast from 330-360 terawatt-hours (TWh) to 300-330 TWh.

The EU-27 generated 1,404 TWh of electricity from nuclear facilities during the period Mar-Sep 2022, down 75 TWh (5%) from the same period in 2021. Generation restrictions as a result of low water levels during the summer drought contributed to the decline. However, it was persistent technical and maintenance issues affecting more than half of France’s nuclear reactors that has dogged nuclear generation.

Remember that France accounts for around 52% of EU-27 nuclear generation. In 2021, nuclear represented 44% of France’s installed electricity generation capacity (61 GW across 56 nuclear reactors), and 69% of its power generation (581 TWh).

EDF’s ability to maintain its nuclear fleet is crucial, not simply for France’s own power needs, but also that of neighbouring countries. When Europe really needed a source of reliable, clean power generation, many of France’s nuclear plants were missing in action.

The drop in nuclear generation could not have come at a worse time for Europe’s energy markets given concerns over natural gas supplies in the aftermath of Russia’s invasion of Ukraine. Hydropower generation (another form of baseload power generation) also proved far from reliable as water levels dropped (see The forgotten giant of clean energy). To fill the gap Europe has had to burn more coal and lignite, import more LNG to fuel gas powered generators and expand it’s solar generation.

As I explain in The sword of inelastic supply cuts BOTH ways, the late summer surge in power prices (French power prices climbed to a record €1,100 per MWh) also coincided with a sharp increase in EU carbon prices to ~€100 per tonne as utilities looked to hedge their power generation while the supply of allowances via auction was limited:

The supply of EUA’s is essentially fixed in the short-term…In August auction volumes are cut by 50%, reducing the primary supply of EUA’s onto the market. Overall then the supply of EUA’s is likely to be highly price inelastic, and especially so during August.

If you combine this with parabolic increases in natural gas and power prices then even a small increase in demand can result in a sharp rise in the price of carbon. Utilities seek to hedge their future power generation by either purchasing allowances, or by hedging that requirement using the carbon futures market.

As we near the end of 2022, what chance is there of a similar scenario occurring in 2023? Again, it may come down to the weakest link in Europe’s energy generation - France’s aging nuclear fleet.

Unlike last year, EDF is now being afflicted by strike action. As of late last week, around one-third of EDF’s 18 French nuclear sites were being affected by strike action. The action by workers has served to delay the completion of maintenance at some facilities by 2-3 weeks, according to some estimates.

Fortunately, there is a way we can get a realistic picture of what the next few months is likely to look like that doesn’t involve trusting the claims made by EDF or France’s politicians.

The next three charts are from Energy Graph. Click on the source link under each chart to go direct to the live data.

The first chart shows French nuclear generation between 2016 and 2021. The purple line at the bottom of the chart shows output during 2022 up until the 18th October (the vertical dotted red line).

You can clearly see that the country’s nuclear generation during 2022 has been significantly below levels seen during the previous six years. Nuclear power output hit a low at the end of August, and although it has rebounded since then, it remains significantly below even year earlier levels.

The stepped purple line past this date shows EDF’s forecast of nuclear plant availability. This is based on their expectation of when plants currently in maintenance will resume generation. However, simply because EDF plan to bring plants back at that rate doesn’t mean that they will.

French nuclear generation 2016-22, MW

You can see the outlook more clearly in the chart below. The stepped line (this time in green) shows EDF’s plan for nuclear availability over the next five months. The line you need to keep an eye on is the yellow one, labelled RTE. RTE is France’s transmission system operator. Every day RTE publish a probabilistic forecast of French nuclear generation.

French nuclear generation forecast, GW

French nuclear generation typically peaks around early February each year. Based on EDF planned availability the country could generate up to 59 GW by February 2023. However, based on RTE’s projection, France is more likely to generate 46.2 GW, putting it around 3 GW lower it was able to generate at the same point in 2022.

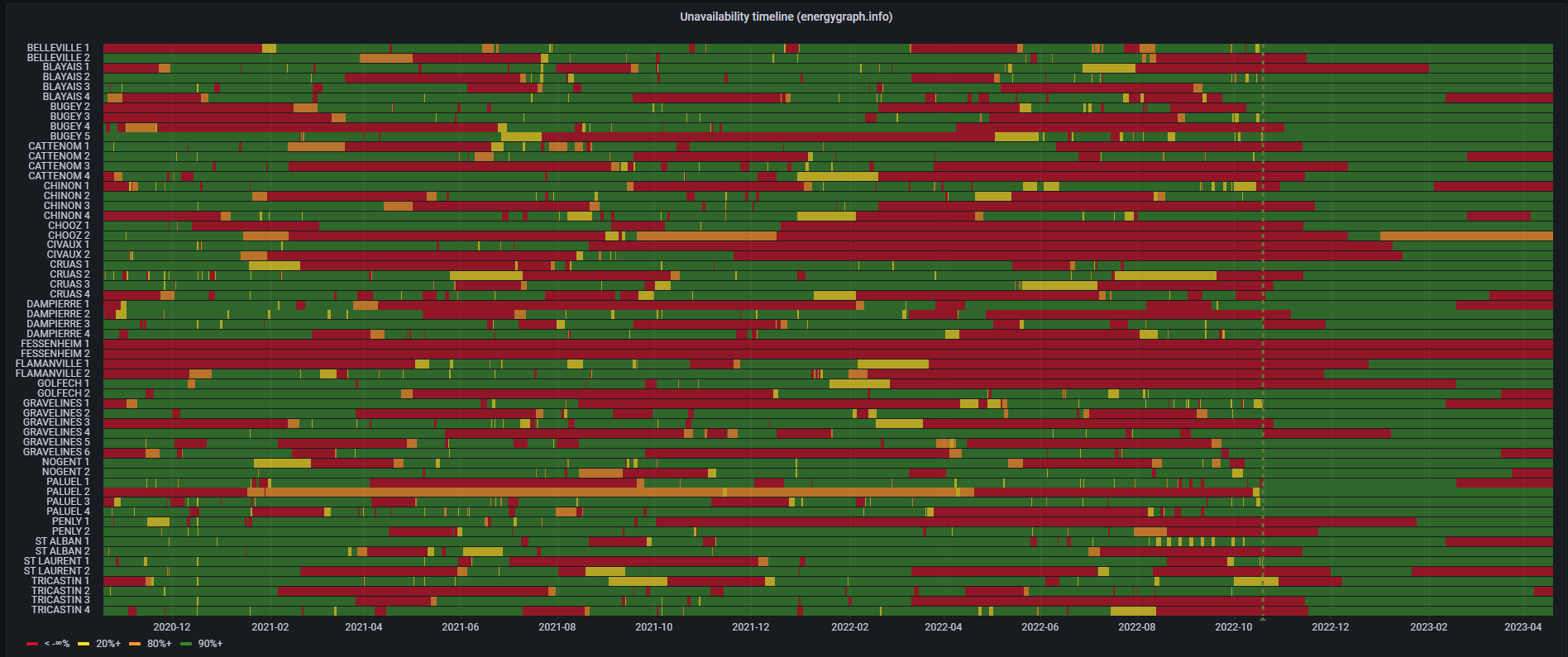

Based on EDF’s schedule, 24 out of EDF's 56 reactors are due to return before the end of the year, while 5 reactors are scheduled to return in early-2023. However, as the chart below shows, from late January onwards, some 14 units are scheduled to come offline for early 2023 maintenance.

French nuclear reactor unavailability timeline

However, RTE believe the situation is likely to become precarious if France heads into peak demand season and EDF fail to resolve the strike action quickly: "A prolonged social movement would have heavy consequences for the key part of the winter."

France’s nuclear reactors have generated about 215 TWh so far this year. Overall, EDF estimate that annual 2022 output is likely to be toward the lower end of the 280-300 TWh range.

France’s nuclear winter of discontent is likely to mean Europe will need to rely on more coal or gas power generation.

In the event that there is a cold snap during late 2022 and into early 2023 (also a time of low EUA auction supply), carbon prices may see another spike as utilities demand for carbon allowances rises.